Beware of Calendar Month Price Predictions

Introduction

It is becoming increasingly common for social-media influencers to predict upcoming monthly returns for Bitcoin (BTC) based on the returns of the same calendar month in previous years. CryptoTwitter (CT) threads and YouTube streams were littered with warnings about how bad a month March 2021 might be based on past March returns, and now hopium is riding high for April 2021 because of how great April returns have been in previous years.

Poppycock.

At least for now.

The Problem

There are at least three problems with trying to predict future monthly returns based on the returns of the same calendar month in years past:

Calendar months do not align with the dates of the halving cycles.

The macroeconomic environment has varied considerably each year.

Market players have changed over time.

The first problem above is the biggest problem, in my opinion. Virtually all BTC bulls believe in the rhythm of the halving cycles, whether implicitly or explicitly acknowledging so. And for those who claim otherwise, then you must disregard virtually all past price action (PA) when trying to ascertain where Bitcoin’s price is headed next. Why? Because virtually every model, metric and indicator floating around cyberspace is based on the halving cycles. Whether the S2FX model, the Pi Cycle Top Indicator, @ecoinometrics price tracking, @ChartsBtc log scale price history, or any of the other dozens of models, metrics and indicators in existence, virtually all have their basis in the halving cycle.

The first problem above should thus be obvious: calendar months fall during different points in each halving cycle. Take the month of March, for example. March 2013 was the fourth full month after the November 2012 halving, March 2014 occurred 16 months after that halving, March 2015 occurred 28 months after that halving, and March 2016 occurred 40 months after that halving (or better stated, occurred four months before the next halving in July 2016). As I will show later, it is this variation in distance from the previous halving (or proximity to the next halving) that matters far more than the calendar month per se.

The second problem is that each calendar month occurs within the context of a different macroeconomic environment. While one could argue that the majority of BTC’s price history has occurred primarily within the context of the single longest bull run in US equity market history, using US equity markets as a proxy for the entire macroeconomic environment would be misguided. First, BTC’s correlation with US equities, and particularly high-growth stocks like those of US Big Tech, has waxed and waned throughout BTC’s history. Second, other exogenous factors have also influenced BTC PA throughout its history, including the relative strength of the USD (often with the DXY being the proxy for USD strength), long-bond yields and isolated macroeconomic events, none more significant of course than the global pandemic of the past year, which incidentally wielded its greatest influence in yet another March, that of course being March 2020.

The third problem with trying to use calendar-month past performance as the basis of future calendar-month predictions is that the nature of the most influential market players has varied over time, which frankly is a problem not only for calendar-based predictions but also halving-based predictions, as I’ve argued elsewhere.

Two recent examples of how market players influence calendar-month performance differently can be found in the PA during recent options & futures expiration weeks as well as quarter-end months like March 2021. In short, given the influence of institutional investors on the PA of this halving cycle in particular, PA has recently been more volatile, specifically encountering downward pressure, in the weeks of options & futures expiration. I frankly still question whether this influence will be long-standing, but the first three months of 2021 all have seen swoons leading up to these expirations, so it is possible this will be an ongoing issue for BTC now that so many institutions, and more specifically institutional traders, have entered the market.

The same is true for quarter-end months (March, June, September, December). While too few data points exist to evaluate whether there is a meaningful correlation with price, it is reasonable to assume that as more institutions enter the market, the greater the impact quarterly portfolio rebalancing will have on price, given that many corporations will have mandates (or at least objectives) requiring that their portfolios maintain a particular allocation by asset class.

Even at the retail-investor level, different market cycles have had different retail participants. For example, East Asian investors more heavily participated in the 2017 bull run than in this cycle to date, with anecdotal evidence suggesting that North American retail investors have participated more this cycle, at least thus far. Given the different cultures, events like the Lunar New Year (typically late January or early February on the solar calendar) may have influenced monthly PA more in the past than, e.g., this past February. The timing of US citizens receiving their government stimulus checks has also clearly influenced retail BTC purchases, with the first $1200 US stimulus check even having its own Twitter handle. In this case, not only have the market participants varied, but exogenous factors (i.e., the stimulus checks) have influenced BTC PA differently and at different points during the calendar year.

For at least these three reasons, trying to use past calendar-month performance to predict future monthly performance is misguided. In fact, I would argue that trying to use past performance at all is in some respects a dubious strategy for trying to gain insight into future PA, which is why I now in fact endorse hodling vs. trading.

Still, the more I have come to understand the Bitcoin protocol, the more I have come to believe in its almost mechanical rhythm. i.e., I have increasing confidence in the nature of the halving cycles - I believe BTC is going to do what it has always done, almost irrespective of whatever noise is circulating at any given moment. As such, I am now an unreserved advocate of the S2FX model despite my background, as well as my acknowledgment of the concerns with the model from a statistical perspective. In short, I see no reason to question the model’s predictions until/unless they break down. Why fight it, especially when it is currently tracking nearly perfectly?

The (Potential) Solution

It is for the latter reason above - my high level of confidence in the BTC protocol and its seemingly inviolable rhythm - that has led me to conclude that if one wishes to use past monthly performance at all when trying to predict future monthly performance, it makes more sense to use distance from the most recent halving (or proximity to the next halving) as opposed to location on the calendar.

By way of comparison, below are BTC’s monthly returns per the BLX ticker on TradingView.com:

As shown in the far right columns of the top table above, literally every month except September has been an up month for BTC throughout its history, at least based on summative and mean (average) values. From these perspectives, it is relatively easy to refute the claim that, e.g., March is typically a bad month for BTC. More specifically, social-media prognosticators typically chose frequency as the base statistic for their predictions (i.e., Is the month more often green or red?), which could be argued to be a weak means of evaluating past performance - that is, unless there is reason to assume calendar months per se have some significance with respect to BTC.

For example, using past calendar-month data to try to predict Berlin’s average temperature this coming August would be completely justified. Temperatures clearly vary by season/month, and there is a well-established and tight range of temperatures in Berlin in the calendar-month of August of past years. However, there is nothing inherent to the Bitcoin network, protocol or market participants that justifies using calendar months to try to predict future monthly price performance. As alluded to earlier, this will likely change over time as more institutional investors enter the market, participants who do indeed make investment decisions based on calendar-specific events (month end, quarter end, holidays, etc.). However, these calendar-based data are only now starting to emerge and thus will be insufficient for modeling/predictions for the foreseeable future.

Equally interesting, though, is the lower table above, which illustrates transposed returns by calendar month. When the data are organized in this way, it is less obvious which years are the so-called bull-phase years. 2013 and 2017 are usually cited as the bull-phase years, and when looking at both the summative and mean (average) returns of these two years, they are indeed. However, they are not obviously so based on visual inspection of the table alone. i.e., One could argue that 2012 is the most bullish year, in that it has had the fewest down months of any calendar year. It just so happens that some of the up months in 2013 and 2017 were so parabolic, they more than offset their respective down months. Regardless, the larger point is this: whether examining calendar-based returns by month across years or by years per se, both strategies are misguided because each BTC halving has occurred in a different calendar month, thereby rendering calendar-based predictions largely meaningless.

To further my point, below are the previous halving dates:

28 November 2012

9 July 2016

10 May 2020

As shown, all three halving dates vary considerably, with two months separating the latter two cycles and over six months separating the first and third cycles. Because virtually every model, metric and indicator has its basis in the halving cycles, it is clearly misguided to, e.g., rely on BTC’s monthly performance in April of past years to try to predict what will happen this coming month.

Instead, it seems far more logical to try to predict the performance of this coming month by comparing it to the months that are equidistant from their respective halving cycle. In this case, April 2021 is 11 months after the most recent halving, which aligns with June 2017 of the previous cycle and October 2013 of the cycle before that.

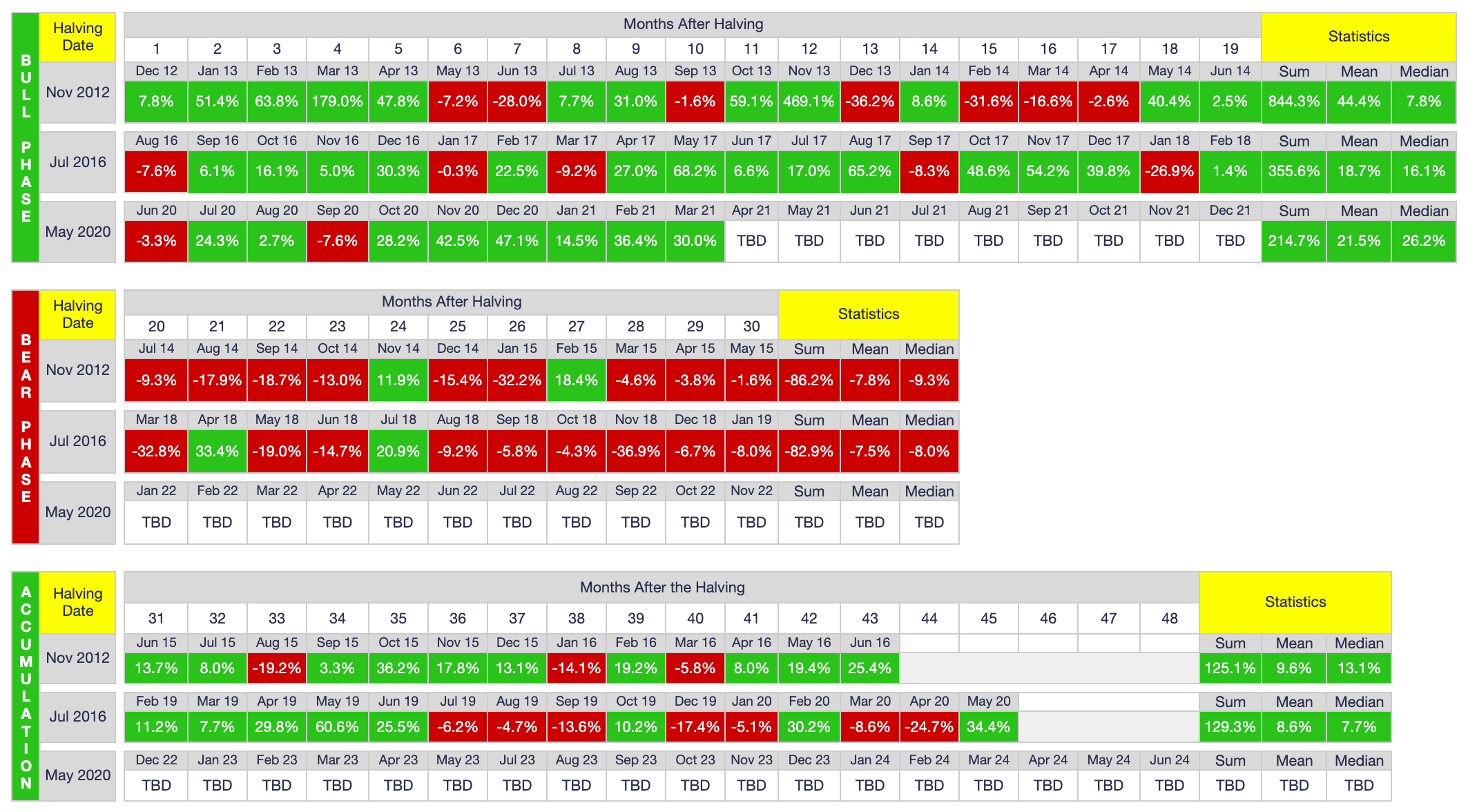

When organizing monthly performance by location within each halving cycle, performance trends become much clearer, as shown below:

As shown above, the first 19 months after the halving cycle have been the most bullish of each cycle, while the subsequent 11 months are horrendously bearish. Each cycle then ends on a surprisingly bullish note, with the final 13-15 months of the cycle, leading up to the following cycle, far more bullish than I had been led to believe, at least in terms of cumulative and mean (average) returns. For example, while there a nearly even number of up (8) and down (7) months to conclude the previous cycle, the final 15 months of the cycle still led to a 129% gain overall, with an average monthly return of 8.6%. This is astounding. 8.6% is a good YEAR, much less a good month!

Organizing the data in this manner also immediately dispels the widely held belief of “one bullish year followed by three years of crypto winter.” This simply isn’t the case. On the contrary, there appears to be a year-and-a-half mega bull run, followed by an 11-month nausea-inducing drawdown, followed by a price-doubling the following 13-15 months. In short, the exact opposite of the commonly held belief is true: each BTC halving cycle is a one-year bear market wrapped inside an incredible three years of otherworldly gains. I even hesitate to label the third phase “accumulation” like so many others have when the cumulative returns of the previous two “accumulation” phases are 125% and 129%, respectively. My, how BTC price action distorts reality.

Conclusion

There are numerous highlights from each of the posted tables that could be discussed at great length, including Month 24, which is the only month of the previous two bear phases to go up in price, and not by a little (11.9% and 20.9%, respectively), but such detailed analysis is for another time. I will close by repeating my themes throughout:

First is that I think relying too heavily on past performance to predict future performance is unwise generally speaking. At most, past-performance data should be only part of own’s analysis when trying to make investment decisions. In my opinion, macroeconomic factors and human psychology play equally if not more important roles in price action, so these factors should also be a part of the decision-making process (to the extent they can be foreseen at all).

That said, to the extent a BTC investor in particular wishes to use past-performance data to try to predict future performance, it makes much more sense, in my opinion, to evaluate halving-based data rather than calendar-based data, particularly when evaluating monthly returns. In this light, below is how the current halving-cycle dates align with the other cycles with respect to the three phases I identified above:

Bull phase: June 2020 - December 2021

Bear phase: January 2022 - November 2022 (but Month 24 is May 2022!)

Accumulation phase: December 2022 - January 2024 (estimate = 14 months)

Whether any/all of these dates end up aligning for a third consecutive cycle is of course an empirical question; we will know for sure in about three years. Until then, I leave you with some final food for thought before you close your browser window:

We just closed our sixth consecutive green monthly candle (March 2021). This win-streak has been equalled only one other time in BTC history (November 2012 to April 2013). I can therefore state with a high level of confidence that we will print a red monthly candle eventually. Consider yourself forewarned.

Based on frequency counts of up months to down months, the current cycle is tracking more closely with 2017 than 2013, the latter of which had seven down months during its 19-month bull phase, whereas 2017 had “only” five down months during its bull phase. As alluded to earlier, this cycle has printed only two red candles thus far (June 2020 and September 2020). On the other hand, the monthly price gains this cycle are tracking more closely to 2013 than 2017, with monthly gains far exceeding those of 2017, as illustrated in many charts on CT, including this one. In short, we are experiencing the best of both worlds right now: big price gains akin to the 2013 cycle but with less downside akin to the 2017 cycle. Will this win-win trend continue? I certainly hope so, but it is important to maintain some perspective about just how truly epic this cycle has been thus far. i.e., Regardless of whether you bought at $6K or $60K, I encourage you to appreciate the truly extraordinary market we are in the midst of, all the while recognizing there is no guarantee it will continue on the same trajectory. In short, by all means continue hoping for and expecting the best, but prepare for something worse just in case.

One final fun fact: neither of the previous two cycles actually lasted four years. As shown in the tables above, the first cycle lasted 43 months and the second lasted 45 months. It is impossible to know in advance how long this cycle will last, but given the incredible hash rate miners have been applying to the network, I suspect this cycle will also end up shorter than four years (48 months) in duration, instead completing in +/- 44 months. If so, that means the next halving would take place in January or February 2024. This prognostication means fairly little at the moment, but historical halving cycle data do to some degree counter the “4-year cycle” mantra we so frequently bandied about on CT and elsewhere.

I guess this is all for now. As always, I will continue to share my personal thoughts on CT regarding BTC’s PA as we forge ahead, for whatever they’re worth. In the meantime, if you have any questions or comments about this article, please let me know via the links below or on Twitter. And as always…

Go BTC.

Awesome article as usual David. Loved reading all those numbers.