Bitcoin Volatility Explained

Introduction

After having studied the price action (PA) and on-chain data of Bitcoin (BTC) pretty closely for the past 18 months, I think I now have a pretty good understanding of the reason BTC is so volatile and often seemingly so unexpectedly.

The purpose of this article is not to identify the catalysts of any particular price spike or swoon but instead to explain how the heterogeneity of BTC’s market participants is what causes such volatility when such catalysts emerge. For instance, it seems pretty clear that the volatility experienced this past Wednesday (November 10) had two catalysts. The first was the higher than expected inflation print that led to an immediate spike in price. Not long thereafter, price reversed course, ultimately giving up all of the gains induced by the inflation print. The most posited explanation for the reversal is a report that Evergrande had defaulted on a bond payment (although the report ultimately proved to be false). In my opinion, demonstrating that the Evergrande default rumor was the catalyst for the price reversal is less convincing than demonstrating the inflation print was the catalyst for the price spike, but no matter. Price ultimately crashed only hours after making a new ATH. Why?

For better or worse, the insight I provide below will be of little value to traders because it does not in any way help infer future price trends. On the other hand, I do think such insight will be of some value to long-term investors, true hodlers, in that having a better understanding of why BTC is so volatile might make the rollercoaster ride a bit less nauseating along the way.

The Heterogeneity of BTC Investors

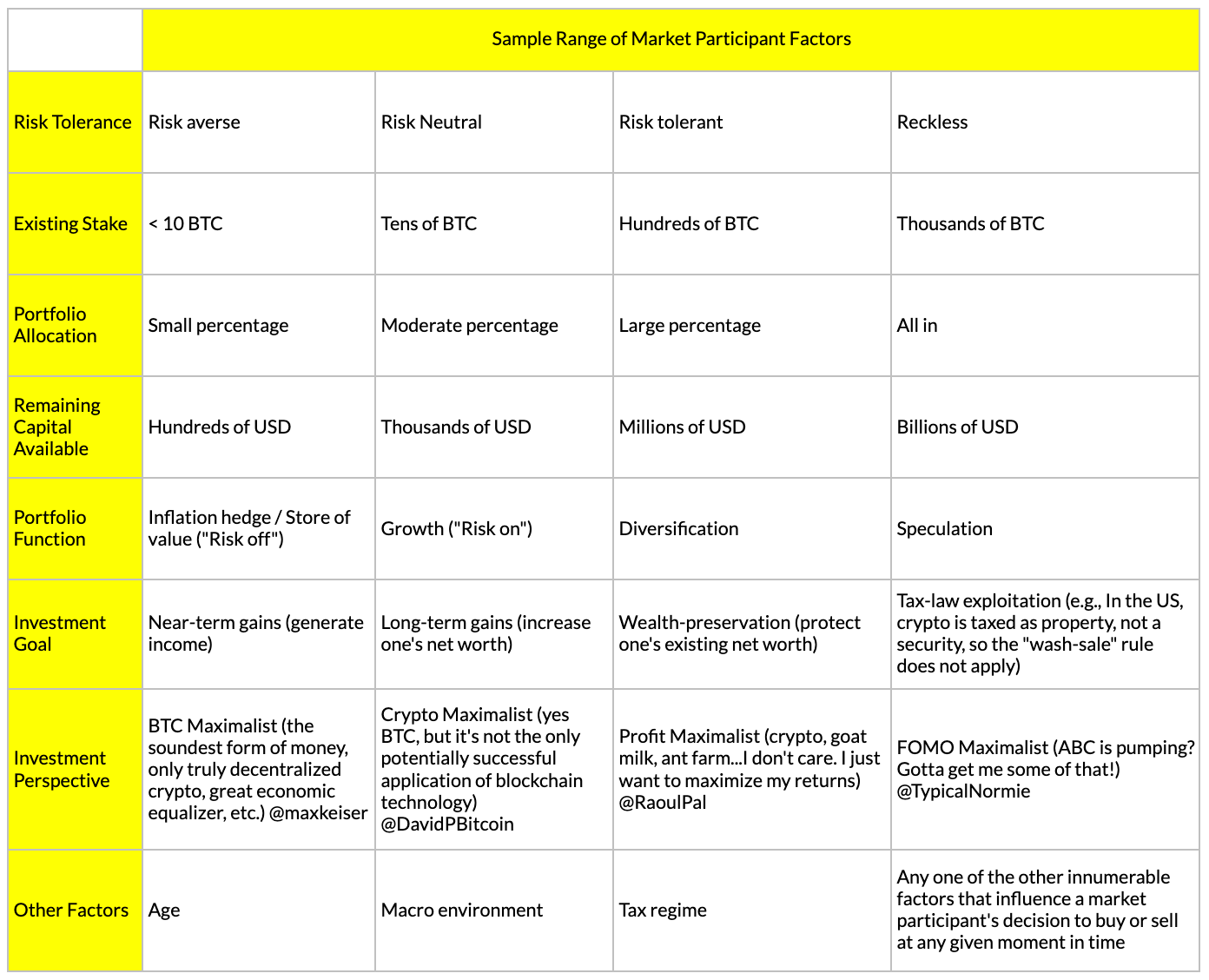

The fallacy to which so many Crypto Tweeters (CTers) seem to fall victim is failing to understand (or acknowledge) that BTC market participants are not homogeneous; not everyone enters the market with the same perspective, capital, risk tolerance, timeframe or profit motives. i.e., While most CTers seem to understand/acknowledge at least nominally that there are bulls and bears, whales and minnows, traders and hodlers, etc., my Twitter feed nevertheless gets inundated with tweets that suggest otherwise every time price moves substantially in one direction or the other. For example, BTC’s Fear & Greed Index would whipsaw far less if more CTers understood/acknowledged just how heterogenous BTC’s investor base really is. Likewise, my Twitter feed would contain far fewer tweets of exasperation every time price swoons and far fewer tweets of euphoria every time price spikes. In short, investor sentiment would be much less volatile if more CTers truly understood/acknowledged the heterogeneity of BTC’s market participants.

Below is a table illustrating the myriad factors that influence BTC market participants.

Note that the cells in the table above are not mutually exclusive, meaning some factors unquestionably overlap. For example, one’s tolerance of BTC price volatility depends in part on how much of one’s portfolio is invested in BTC. If only a small percentage, then one’s tolerance is likely to be higher than if a larger percentage is invested. Moreover, investor perspectives often change over time. For example, one may initially buy BTC as a speculative investment, hoping to generate outsized near-time gains, but then end up investing for the long term once they begin to better understand the protocol and its potential. This latter example in particular is the reason BTC’s price floor is monotonically increasing.

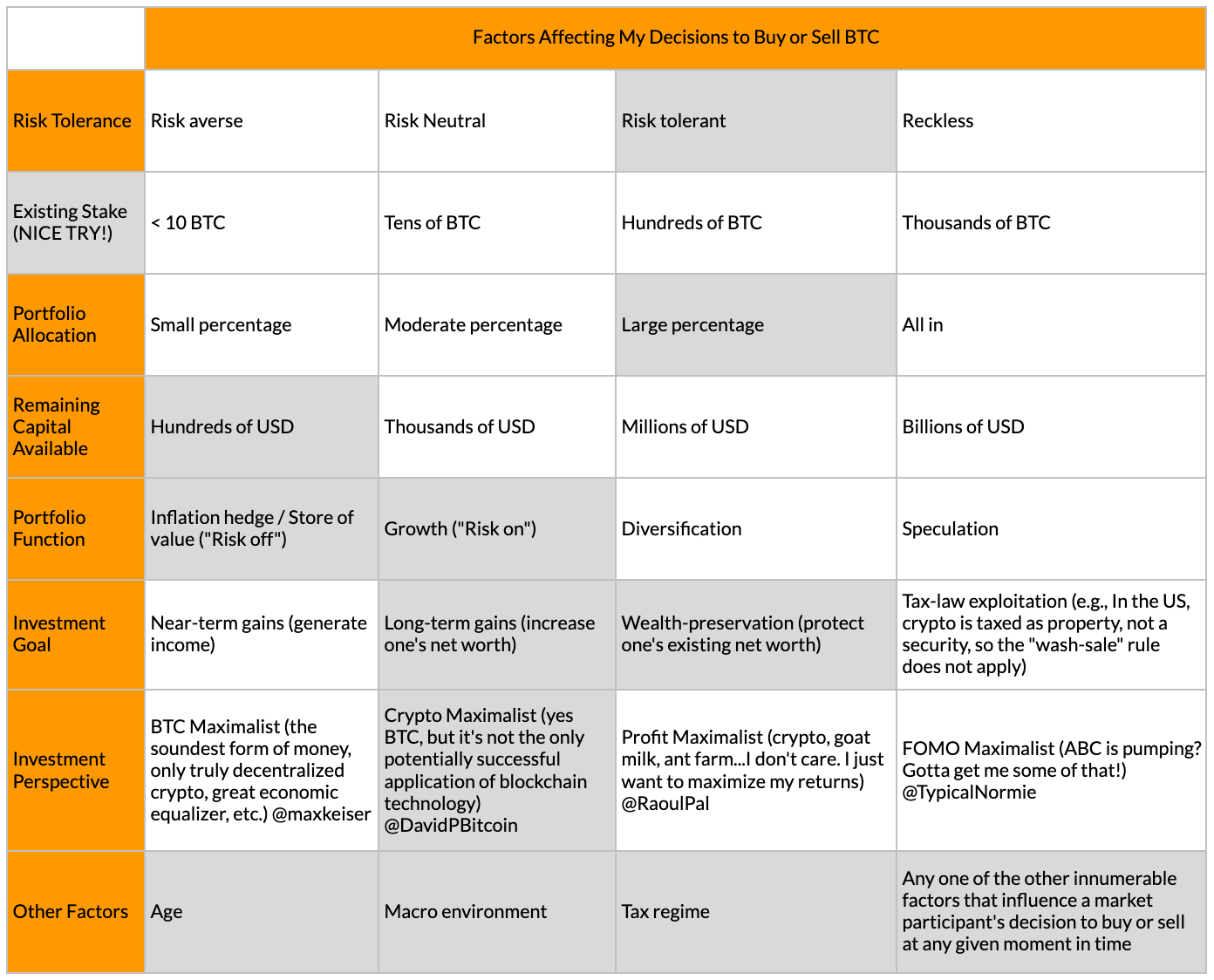

To help crystallize understanding of this schema, below is my own profile.

As shown above, I consider myself risk tolerant, although I will say that is due in part to my increasing knowledge of and experience with BTC over the past 18 months. I also now have a large percentage of my net worth in BTC, with little left to invest either now or in the future because I am retired. That said, I have invested in BTC because I consider it the perfect asset - an inflation hedge by design but early enough in its adoption that exponential growth is still possible. More on this later.

Continuing on, my goals are both to increase my net worth and preserve my existing wealth, the balance of which is probably the greatest challenge I confront as an investor. Finally, I consider myself a BTC maximalist in spirit, but ultimately I believe the crypto space is not a winner-take-all, zero-sum game, such that I think other blockchains can/will simultaneously flourish. I thus own some ETH, DOT, ADA and ATOM, although BTC remains (and likely always will be) my largest holding by far.

As you can also see above, I highlighted all of the cells in the Other Factors row, including my age (although I am retired, I am still relatively young, so I theoretically have a longer-than-average time period for which I must preserve my wealth). I also monitor the global macro environment closely, although honestly it rarely factors into my investment decisions these days. Finally, and perhaps most importantly, I moved to Puerto Rico to avail myself of tax incentives offered to mainland US citizens who relocate to the island. This is a critical factor that will heavily influence my future investment decisions.

The reason I share my own profile is to illustrate three points: 1) we each have our own unique investor profile (what is yours?); 2) investor profiles change over time; and 3) there is a greater variety of factors that influence BTC market participants than participants in most other markets. In other words, BTC market participants are extremely heterogeneous, spending more time in conflict with each other than in synchronicity. Hence the reason parabolic spikes like that of Nov-Dec 2017 and epic collapses like that of March 2020 are so rare. It is not often the vast majority of BTC market participants think and act in unison. Instead, they spend far more time competing rather than cooperating.

But isn’t this true of all markets? Not exactly. In more mature markets, there is a much cleaner demarcation between buyers and sellers. No such demarcation exists in BTC’s market. BTC’s market is more like a royal rumble than a tug of war.

In other words, most other markets have two well-defined opposing forces: the bulls and the bears. Take the JPM market for instance. At any given moment in time, some percentage of JP Morgan’s market participants will be bullish on its future earnings, growth, etc. while the complementary percentage will be bearish. If more participants are bullish, its stock price will increase; if more are bearish, then price will decrease. Moreover, because JP Morgan is a mature company with future expectations that are reasonably well-defined/predictable, its stock price will be relatively stable over time (at least in the absence of any so-called black swan events).

The BTC market on the other hand could not be any more different. Price oscillates not only more frequently but also more violently and often more unpredictably. With BTC, it is hardly ever a simple matter of whether market participants are more bullish or bearish. If it were, price would be both more predictable and less volatile than it is. But it isn’t. Why? Because of the myriad factors I delineated in the table above, but particularly because of the Portfolio Function row of factors.

As highlighted above, the biggest reason BTC is so volatile is because it is still viewed so differently by so many different people. To some, it is an inflation hedge. To others, it is a growth asset; to others still, it is a diversifier (portfolio insurance, if you will). And of course there are always the reckless speculators.

Add these chasm-wide differences in perspective to the basket of more common market participant differences and you get a royal rumble rather than a tug of war: multiple market participant types simultaneously battling for supremacy, which is what leads to the chaos that is BTC price action.

An Illustration

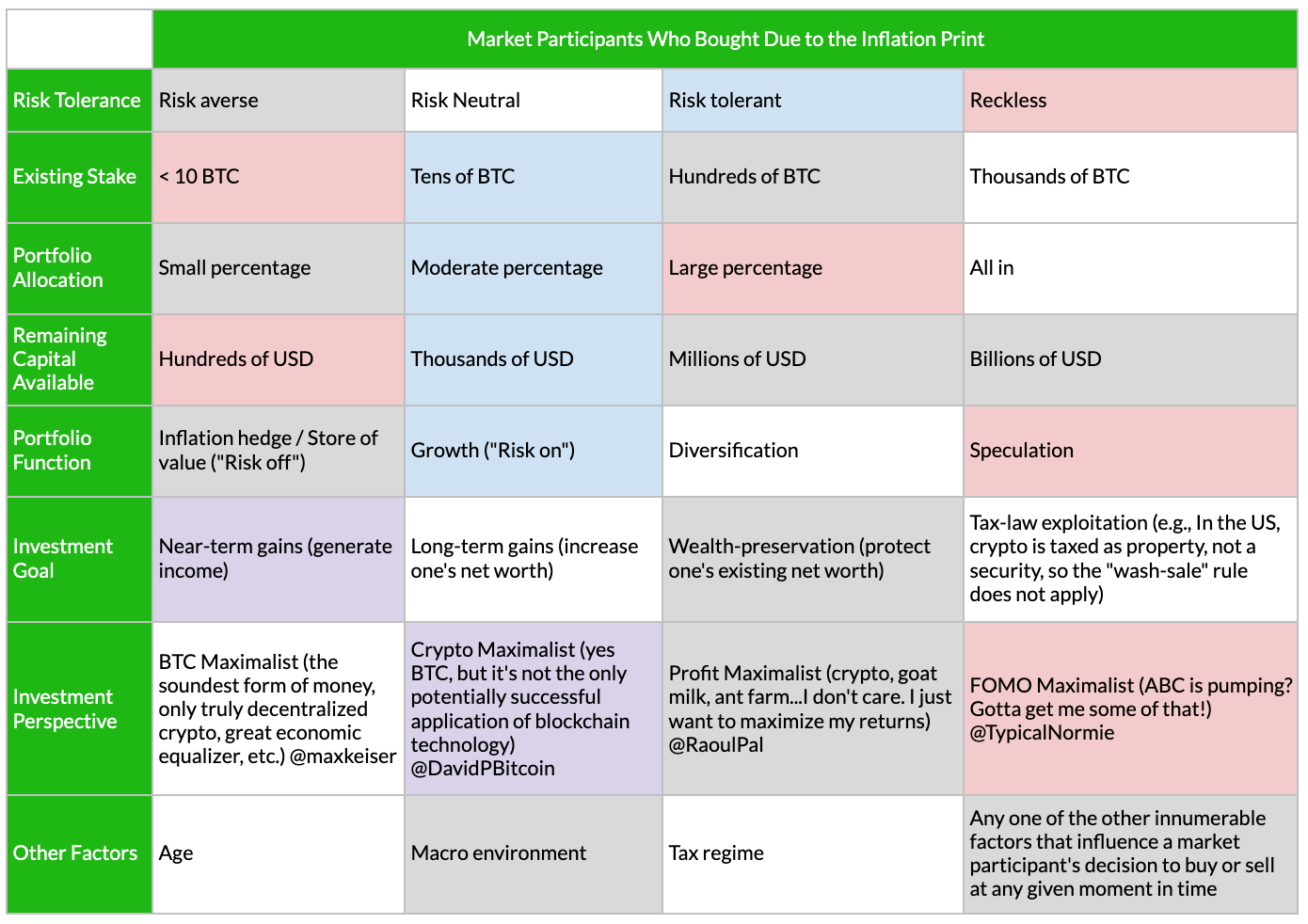

To illustrate my point about the conflicting heterogeneity of BTC market participants, following are two more versions of the same table, the first of which illustrates the three investor groups that I think bought when the inflation data were released.

Unfortunately, I lack the time, patience and skill to create a more visually accurate representation, but let me explain what I am trying to illustrate. First are the gray boxes that represent one group of investors. This group comprises primarily US institutional investors, some of whom may already have substantial stacks, but either way whose BTC position as a percentage of their assets under management is quite small. They have millions (or even billions) of USD available for investment, so when inflation printed hot, they immediately bought inflation hedges, BTC being one.

In the event anyone questions whether it was actually the inflation print that caused the spike, just look at the chart below.

The inflation data were released at 08:30 Eastern Standard Time (13:30 UTC). Price skyrocketed immediately thereafter, rising $2,700 within 45 minutes. Moreover, look at the volume bars at the base of the chart - a massive spike in volume occurred at 08:30 EST, made possible only by large sums of capital suddenly flowing in. i.e., US institutional investors were the primary buyers at 08:30 EST, undoubtedly aided by algorithms that help identify and capitalize on such macro data anomalies.

While many CTers were high-fiving each other due to the new ATH reached that morning, I personally was far more gratified by the realization that for the first time I can recall, a number of US institutional investors clearly now view BTC as an inflation hedge. This is the real news, in my opinion. While many people have long conceded that BTC is by design an inflation hedge (cap of 21M coins, halved inflation rate every four years, current stock-to-flow ratio relatively comparable to gold), more investors still seem to view BTC as a speculative growth asset, and not without good reason: it is after all still a 70-vol asset with PA more akin to a tech IPO than that of the longest-running inflation hedge in existence (gold).

While US institutional investors ignited the rally at 08:30 EST, it appears momentum traders (the blue boxes above) started buying soon thereafter, particularly after the former ATH was eclipsed. Finally, by 09:15 EST, full-on FOMO was in effect, with retail speculators (the red boxes) aping in (look at the size of the green volume candle at 9:15 EST in the chart above). Again, my table is sorely lacking visually, but for what it’s worth, the purple boxes are factors that I think influenced/characterize both the momentum traders and the retail speculators.

It would take some time studying the table above to fully digest the profiles of each of the three groups I suspect were the primary buyers during the price spike, but the larger point is this: for this brief 60-minute period, simultaneously demand from buyers across a variety of investor profiles overwhelmed the available liquidity on exchanges, so price spiked. It’s just that simple.

Of course, as shown above, the opposite started unfolding only three hours later, commencing at 12:39 EST and ending about 16:30 EST, when price bottomed near $63K, exactly where it had started eight hours earlier. Coincidence? I think not. But note that I think there is only partial overlap between the buyers that drove price up and the sellers that drove price back down. As shown below, while I think the momentum traders (blue boxes) got stopped out along with the retail speculators (red boxes), I also believe at least some of the original inflation-hedge buyers held firm even after price rolled over. i.e., If it wasn’t the inflation-hedge buyers that caused price to fully retrace, then who did? Leveraged longs.

As explained by several people (e.g.), once the price reversal picked up some steam, leveraged long positions also got liquidated, which, if you have been a BTC market participant for anything other than only the past few days, is now a familiar sight. Regardless, the point is that liquidated leverage always exacerbates price reversals, in both directions, leading to what are more colloquially known as “long squeezes” and “short squeezes.” A long squeeze is what punctuated this particular swoon, starting about 16:00 EST and ending 30 minutes later, when price began stabilizing around $63K. Below is a table summarizing who I think the sellers were during the swoon.

Note that I am NOT suggesting that no inflation-hedge buyers sold once price rolled over. Of course some did, which is why I highlighted some boxes above in light gray. But I would also argue that it wasn’t all of them, or even a majority of them. If they all had, then price would have fallen far more deeply than it did, especially with so many leveraged long positions still open further down the price continuum.

The Larger Point

I illustrate above the variety of market participants that contributed to Wednesday’s volatility to make this larger point:

The reason BTC is so volatile is because its market participants are far more heterogeneous than those in most other markets. With BTC, it is rarely ever only a battle between bulls and bears. It is a royal rumble rather than a tug of war.

Understanding and fully internalizing this fact - that BTC is and will continue to be very volatile until its market matures - is critical to helping mitigate the emotional volatility that often accompanies BTC’s price volatility. It should go without saying that investing decisions should be made rationally/unemotionally. Stated differently, making emotionally driven investing decisions hardly ever ends well, whereas the opposite has repeatedly been shown to lead to success. As such, I encourage you to recall the following if/when you find your emotions getting the best of you:

Every transaction requires a buyer and a seller. Ideally both buyer and seller benefit from their transaction. Given that BTC investors have a wide range of investing profiles, transactions need not be zero-sum, winner-take-all affairs. Both buyer and seller can win, especially in a heterogeneous market like BTC.

PA is always a matter of perspective. While falling prices are disdained by those already invested, they are welcomed by those still looking to buy. Likewise, increasing prices are welcomed by those already invested while would-be buyers wring their hands, not knowing whether they should ape in or remain patient. Long and short, price action is never good or bad; it is simply a reflection of the current supply-demand equilibrium. In this respect, I have always appreciated real estate market terminology. Housing markets aren’t “bullish” or “bearish;” they are either “buyers markets” or “sellers markets.” Why equity/crypto markets don’t adopt these terms, I have no idea. Doing so would instantly change the way we view PA. In this light, try to align your future buy/sell decisions with reliable BTC metrics (e.g., Mayer Multiple, MVRV, Pi Cycle Top Indicator, to name but a few). i.e., Buy in buyers markets, sell in sellers markets, and simply ignore all the noise in between.

If ignoring the noise becomes impossible, change your perspective from, e.g., “Oh no, price is collapsing again.” to “I wonder which investor groups are selling and why?” i.e., Turn such volatility into a learning opportunity, an opportunity to better understand which investors are moving the market and for what reason(s). By turning such volatility into an academic exercise, it should help you remain more emotionally detached, thereby helping you avoid making any knee-jerk investment decisions in response.

Finally, if all else fails, knock off the zeroes. I tweeted this strategy once, so some of you may already be familiar with it, but if not, what you do is this: imagine BTC has a board of directors that authorized a 1:1000 split, such that price heretofore will be, e.g., $64.00 a coin rather than $64,000. Then, when, e.g., price increases from $63 to $69, only to collapse back to $63, all within a matter of hours, you will more likely simply be curious about what happened rather than feverishly scanning CT, YouTube and elsewhere trying to figure out what it all means, whether the world will soon end and what you should do about it if so. I’m not kidding. This really works. Knock off the zeroes.

Conclusion

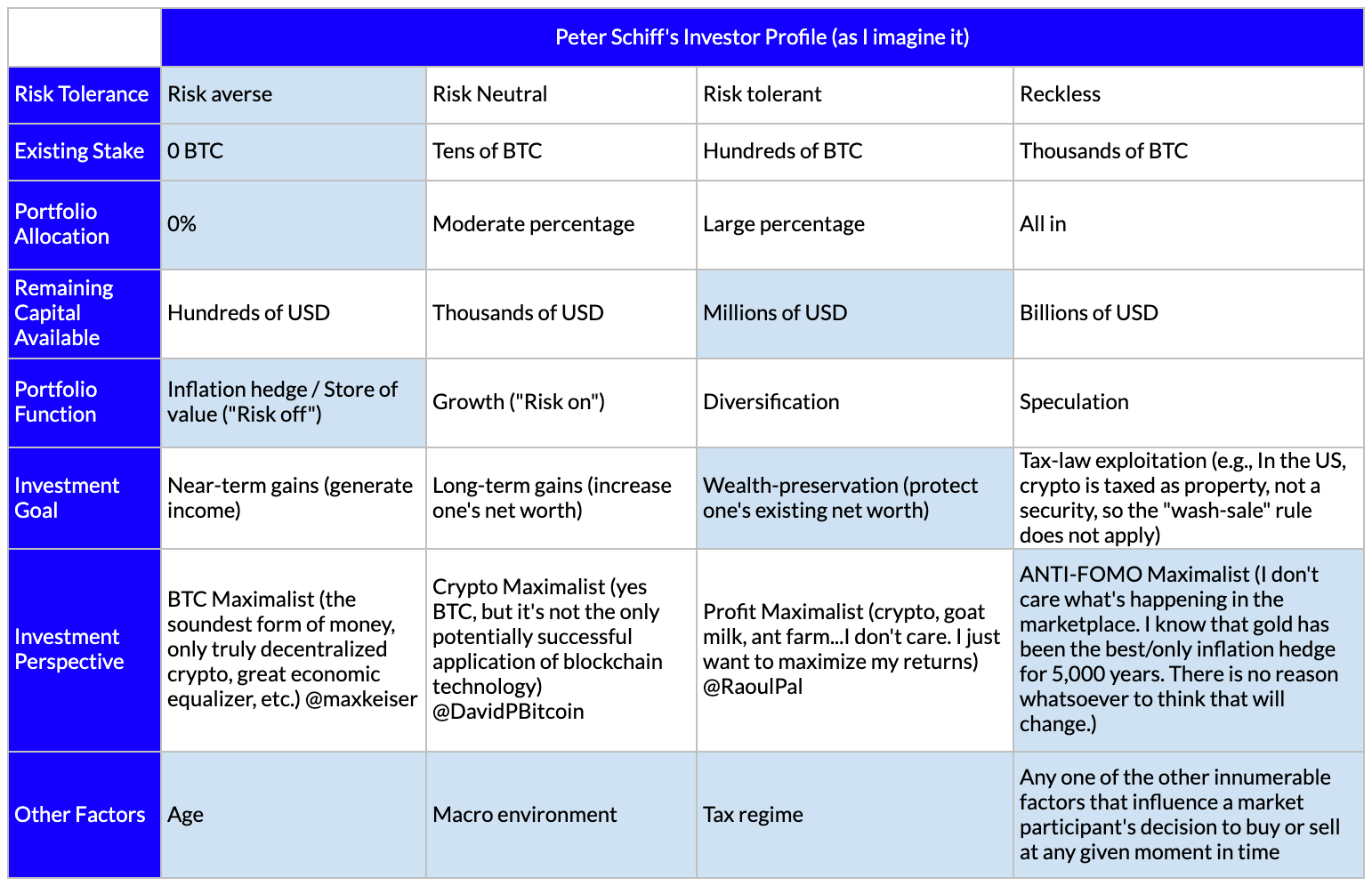

I don’t know Peter Schiff at all. Never met him, likely never will. But based on his public statements about gold and Bitcoin among other things, I imagine his investor profile to look like the following:

Whatever you think of my characterization of his profile, I do believe he is the best investor to test my own beliefs against because he and I should have very similar investor profiles. i.e., While I think my risk appetite is likely greater than his, this is no doubt due in part to the fact that he is already exceptionally wealthy while I continue walking a fine line between remaining comfortably retired and having to return to work to maintain the lifestyle to which my family has become accustomed. In short, I seek growth as well as wealth preservation, whereas I imagine his primary (if not sole) focus at this point is protecting the purchasing power of the wealth he has already accumulated. To this end, he has a point: gold has an unparalleled track record of being a reliable store of value for all of the briefest periods of time over the past 5,000 years. Why should he entertain BTC as an investment? There simply is no reason (yet). So if his logic is sound, then why I shouldn’t I also own gold?

Interestingly, I exited this thought exercise more invigorated than ever about my own investment in BTC, despite no longer having an income source and having only just enough wealth to retire while still maintaining my family’s standard of living. i.e., If wealth preservation must necessarily be my primary investment goal, why would I choose BTC over gold when BTC is so volatile? Because of days like Wednesday.

Yes, Wednesday’s PA concluded on a sour note, exacerbated by the fact that the faceplant occurred only hours after setting a new ATH. Moreover, many of you know I consider growth in the number of whales to be the most reliable indicator of future PA, something that clearly is not happening at the moment, as I illustrate via my daily on-chain data distribution updates. As such, I have as much reason as anyone to be nervous about future PA. Nevertheless, it is now indisputable that at least some US institutional investors see BTC as an inflation hedge. I frankly had always believed it was only a matter of time before BTC began fulfilling its destiny as the ultimate inflation hedge, but Wednesday provided the first tangible evidence that its destiny is in fact beginning to be fulfilled. It is for this reason more than any other than I believe I have made the right choice investing a large percentage of my net worth in BTC. Yes, it will remain volatile until its market participants become more homogenous, but I also think BTC will eventually prove to be the greatest inflation hedge the world has ever known, and there is now incontrovertible evidence that some large, very successful investors are starting to agree. It will just take some time before the balance of power permanently tips in favor of the inflation-hedgers.

In short, I am liquid enough at the moment to support my family, which enables me to ride the BTC rollercoaster day in and day out, hour by hour, minute by minute. I am thus left only having to manage my emotions, which has become far easier since I came to better understand the mechanics of BTC’s legendary volatility. Hopefully this article will help some of you also gain a better understanding of it, thus enabling you to better manage your own emotions going forward.

Go BTC.

P.S. If you are a relative newcomer either to BTC or to my feed, I encourage you to read this article and this article. Although some of the content is dated, the majority remains relevant and the two articles combined will help you better understand the lens through which I view BTC and my investment in it. Whatever you decide to do, good luck with your own investing!