Diversify? Into What?

Why Bitcoin really is the only investable asset at the moment

Preface

Let me start out by saying I have an almost unshakeable confidence in Bitcoin’s future, so much so that, in the absence of a fatal network threat, I believe it will become the world’s premier reserve asset and quite possibly the world’s primary currency one day. That said, I do see the potential for other cryptocurrencies to fulfill a complementary role with respect to storing and transferring value across time and space. Nevertheless, I refer only to Bitcoin throughout this article (as the de facto flagship cryptocurrency) when comparing crypto assets to other potentially investable assets. Stated differently, I think the thesis I unfurl below is relevant to any crypto advocate, whether your allegiance is to Bitcoin, Etherium, Cardano, Polkadot, none of the above, all of the above or a different cryptocurrency entirely.

The Precarious State of Global Markets

My crypto holdings are deep in the money at the moment. I share this fact not to boast but because of the unfortunate realizations such profitability has birthed. First is that I thought it would be easier to manage swoons once comfortably profitable, but no: weird as it sounds, it actually feels worse in some ways to watch profits evaporate during a swoon than it does to be underwater, realizing that profit could have taken off the table had I chosen to. That said, the more spike-swoon mini-cycles I endure with Bitcoin, the more confidence I gain that it is going to do what it does, do what it has always done, irrespective of the noise that surrounds it at any particular moment (see my pinned tweet for more on this thesis). For this reason, I am convinced that the bull phase of the current Bitcoin halving cycle still has a lot of runway in front of it, so I fret not. Profit-taking will have its day. But that’s actually the problem.

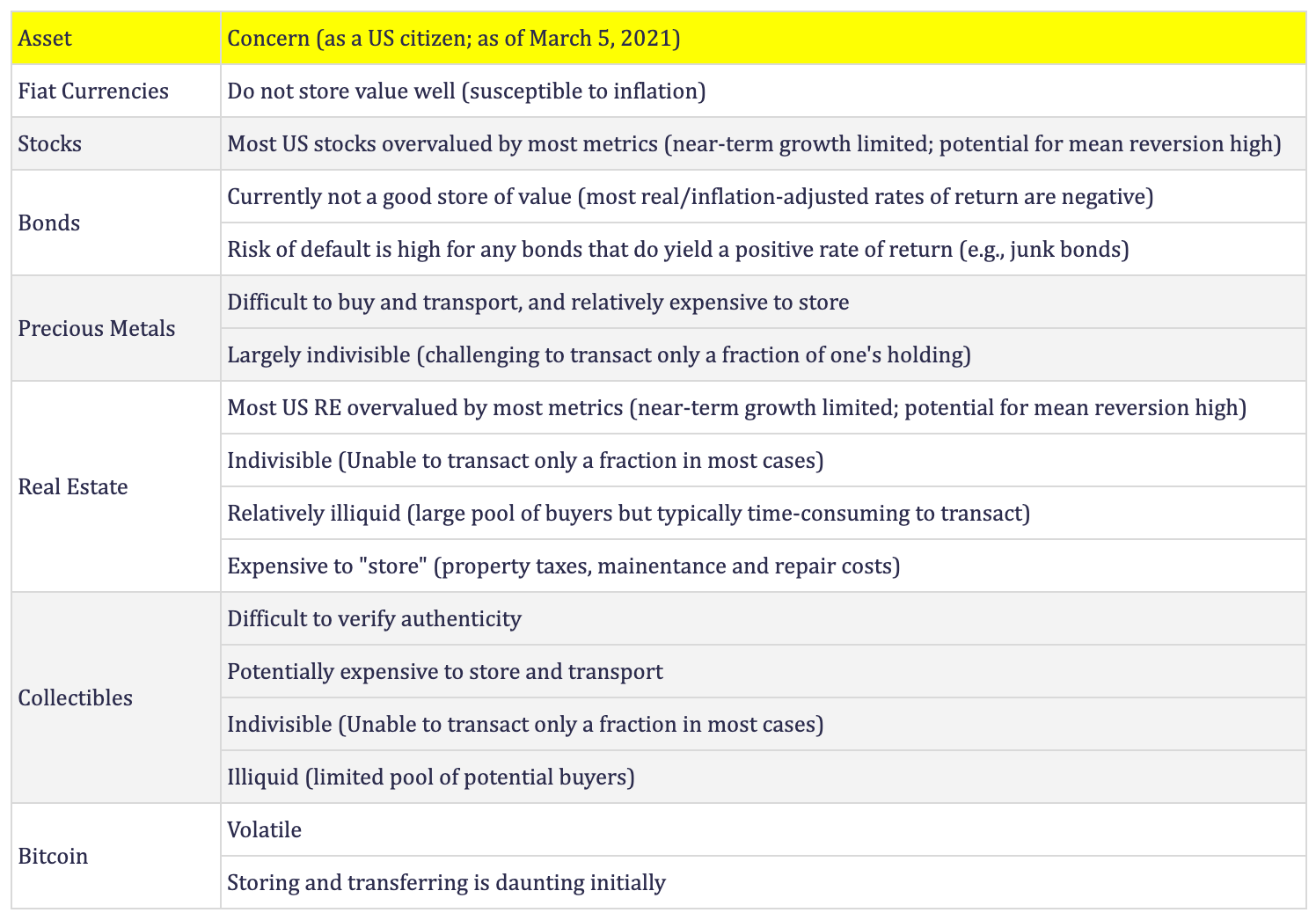

The second unfortunate realization I have come to is that Bitcoin is (or soon will be) just about the only investable asset on the planet for the foreseeable future. This may sound like a preposterous statement, but it isn’t. Believe me, I have looked high and low for viable alternatives in order to diversify my portfolio and there simply aren’t any at the moment. Consider the following:

Note that the concerns I list above are only a few of the many; they are also to some degree specific to my circumstances as a US citizen. Still, I think they apply to most investors at this point in time: there really are no viable alternatives to Bitcoin right now if seeking to protect wealth/preserve purchasing power. I, perhaps for the first time, finally understand why @michael_saylor is constantly looking under the cushions for spare change to buy more Bitcoin. Yes, Bitcoin is volatile, and yes, its storage and transfer is somewhat daunting initially, but for wealth I likely will not need access to any time soon, is there really a viable alternative? Certainly not US equities (stocks): most are overvalued by virtually every known metric, and even if US equity markets don’t ultimately collapse, their upside is extremely limited for the foreseeable future. Conversely, the likelihood of a correction is very high. All assets revert to their mean eventually; so too will US stocks.

But couldn’t the same be said of Bitcoin? No. Many so-called experts try to make this claim, but there are two critical differences between Bitcoin and most US equities:

1) Bitcoin is in the middle of its halving-cycle bull phase, with the bull phase of the three previous cycles each occurring within a different macroeconomic environment. In other words, history demonstrates conclusively that the rhythm of the Bitcoin halving cycle ebbs and flows predictably, almost mechanically, regardless of any noise that causes short-term price fluctuations along the way. Unless/until this rhythm is interrupted, there simply is no reason to question whether it will continue.

2) Bitcoin is still at an early stage of its innovation adoption curve, with only about 2% of the population currently invested in or transacting with Bitcoin. In other words, while most US stocks have already reached market saturation (in terms of investor participation, not the company’s market dominance per se), Bitcoin is still very early in its adoption, particularly with respect to institutional investment. In fact, I would argue that Bitcoin is actually at the ideal point for long-term investment: it is no longer speculative (the Lindy Effect suggests Bitcoin’s future is more assured with each passing day), yet its adoption is still nascent enough that significant future price appreciation seems all but assured (NB: Bitcoin’s location on its adoption curve is one of the primary reasons I believe its risk-reward ratio is unmatched vis-à-vis other cryptocurrencies: the potential rewards may be higher for other cryptocurrencies, but they are all still very speculative, IMO, and therefore much more suited to swing-trading as opposed to long-term investing).

For these two reasons, I would argue Bitcoin is nowhere near as “bubblicious” as the US tech stocks to which it is so routinely compared. Put another way, while I think it it is reasonable to argue that Bitcoin is no more immune to the macro environment than any other asset, I also contend its current valuation is bubbly only in part.

If looking beyond stocks, then, for a portfolio diversifier, a number of concerns emerge: other potentially investable assets are either poor stores of value (fiat currencies, bonds), or even if a traditionally good store of value, they have several disadvantages when compared to Bitcoin. For example, precious metals like gold are difficult to buy and transport, expensive to store, and not easily subdivided. Real estate, also typically a good store of value, is relatively illiquid and expensive to “store” (due to taxes, maintenance and repair costs, not to mention being relatively time/labor-intensive, especially income-producing properties). Real estate is also difficult to subdivide, if it can be at all. The same is true of most collectibles (art, cars, watches, wines), which can be good stores of value but are fraught with risk with respect to verifying their authenticity. Collectibles also have relatively illiquid markets, with only a small pool of buyers within any one market, and they too typically cannot be subdivided easily, if at all.

In short, what I have come to realize is that Bitcoin is just about the only viable long-term play at the moment, despite my desire to diversify. The only potential alternative seems to be other cryptocurrencies, but as I explained earlier, I see most altcoins as more suited to swing trading rather than investing per se because they are still too speculative. And while stocks are often investable, most are overvalued at the moment (at least US stocks), and are thus more likely to revert to their mean rather than appreciate much more. Bonds? Virtually all bonds have negative real (inflation-adjusted) yields at the moment, so they are a no-go. And even other hard assets aren’t really viable alternatives to Bitcoin given how illiquid, indivisible, and/or expensive they are to store, especially relative to Bitcoin. Last but not least, “cash is trash,” as Ray Dalio has been known to say. Governments/Central Banks worldwide are continually debasing their respective fiat currency, particularly those that can issue currency-denominated debt, and none is doing so more aggressively than the US. As such, swapping crypto gains for USD is a non-starter, particularly when accounting for the obscene capital gains tax I would have to pay upon sale. i.e., If I cannot flip my proceeds into another asset that will not only outperform Bitcoin, but do so after accounting for the capital gains tax I would incur upon sale, what possible justification could I have for selling in the first place?

For the time being, I do derive some solace in the fact that the bull phase of Bitcoin’s current halving cycle is fully in tact and should remain so for at least another six months. However, at some point, many of us will inevitably be confronted with an ugly reality: white-knuckle our way through the next Bitcoin bear phase or try to sell near the cycle peak to avoid that nausea-inducing swoon. But to what end?

While I reserve the right to change to my mind, my plan at the moment is to try to time the top of the bull run, selling half of my position and letting the other half ride, presumably forever. But make no mistake. Even if I sell half my stack, my sole goal will be to accrue even more Bitcoin during the bear phase, NOT to diversify into other assets. I simply do not see any other assets being investable at any point in the foreseeable future. The only question, then, is whether the next bear phase will be deep enough to justify trying to sell near the top. I in fact argue that it may not be, and I am not alone in my sentiment. And if it isn’t? You can rest assured knowing I will kick myself all over again, just like I have every other time I have sold in the past.

Go Bitcoin.

I will continue contributing in whatever way I can. Thanks for the feedback!

Thanks for your input in this space David. As someone new to Bitcoin, I find your daily tweets really informative in helping to understand the macro environment. Please keep it up!