Month-End Analysis (and a whole lot more)

November 2023

Disclaimer

The data I use (BitInfoCharts, Coinglass, CoinMarketCap) to compile the tables and graphs contained in the on-chain section of this analysis do not always align with data found via others sources like Glassnode and CryptoQuant. I cannot explain the reason for the differences nor can I confirm which sources are most accurate. For this and other reasons, I have come to trust only the on-chain data I collect when trying to explain and/or predict Bitcoin’s (BTC) future price action (PA). Whether you too find my on-chain analysis useful is for you to decide, but I can assure you some of my observations and/or predictions will differ, often markedly, from other observations and/or predictions you will see on Crypto Twitter (CT) and elsewhere.

Price Action

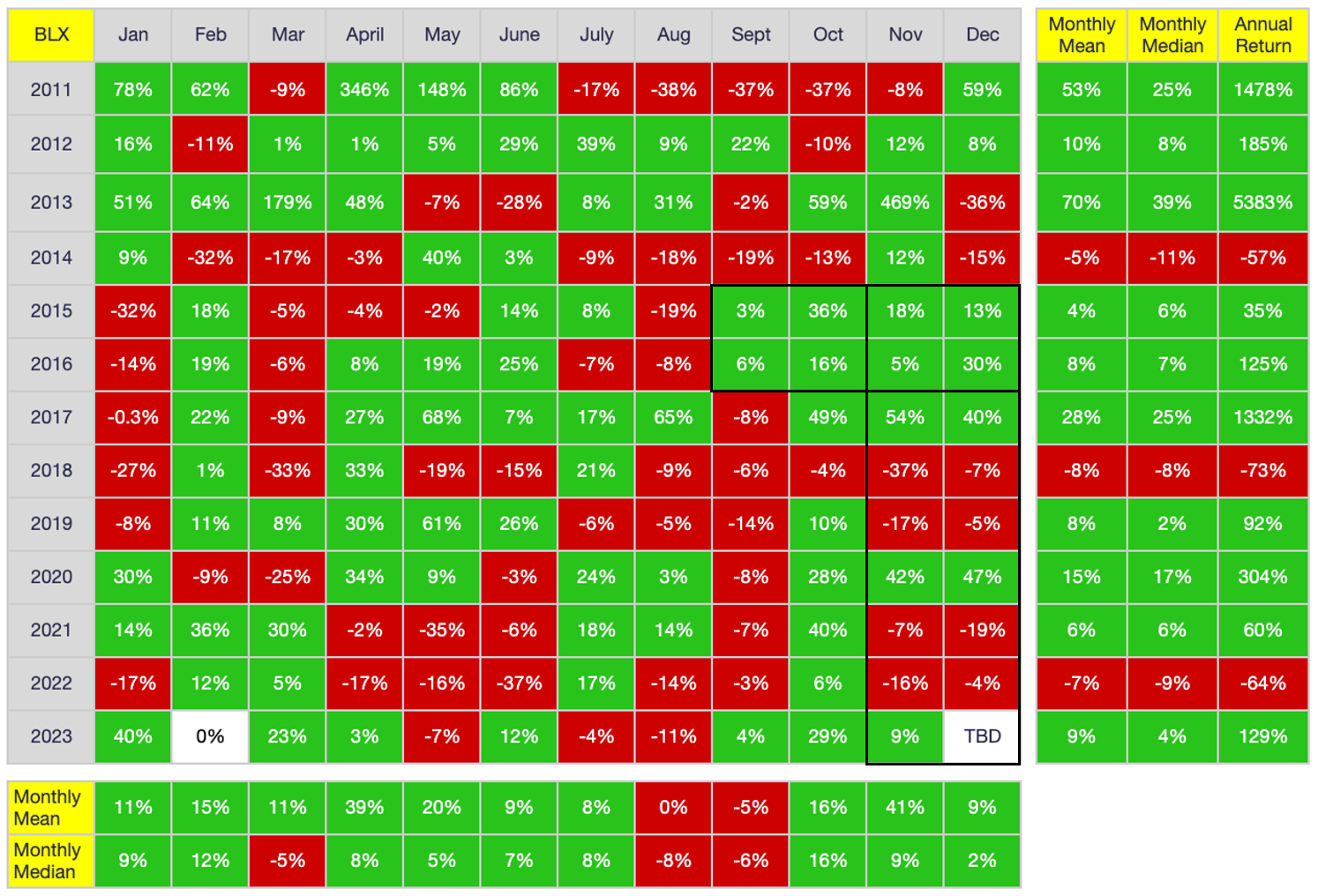

I cannot speak for others, but November seemed like a long month, presumably because of the epic tug-o-war at $38K that occurred the final third of the month. Price opened November at $34,653 (on BLX) and generally trended higher throughout the month, peaking at $38,400 on three separate occasions (November 24, 28, 29) before finally closing at $37,863. When all was said and done, price closed 9.24% higher in November, the third up month in a row:

As shown above, 2023 has been a spectacular year following the misery that was 2022. Year-to-date, 2023 has the highest annual return of any non-halving year since 2012. Moreover, as I highlight above (in black rectangles), the last two times September, October and November all printed green (2015 and 2016), so too did December. Equally interesting is the fact that November and December have traded directionally similarly every year since 2015: when November prints green, so too does December (and vice versa). Combining these two trends suggests that December 2023 should trade higher, at least if you believe calendar-month trends have any predictive validity.

As I have often stated, I generally do not believe in the predictive validity of calendar-month trends (aka, seasonality), primarily because of the low participation rate of large institutions thus far (e.g., US equities unquestionably trade in a seasonal manner due to heavy institutional investment). While this will likely change with the approval of one or more US spot-BTC Exchange Traded Funds (ETFs), here-to-date it has made much more sense to forecast future PA based on the rhythm of the halving cycle.

As shown above, I reorganized calendar-month returns into three identifiable phases of each halving cycle: the bull phase (the first 18 months post-halving), the bear phase (the 12 months following the bull phase) and the accumulation phase (the 15-18 months prior to the subsequent halving). As shown, November 2023 is the forty-second month of the current halving cycle, the twelfth month of the current accumulation phase, and about five months prior to the next halving (projected to occur in April 2024).

While the current halving cycle is trending very similarly to the two previous cycles, I personally think it is trending more similarly to the first halving cycle (2012-2016) than the second (2016-2020). Whether true or not, there is plenty of reason for optimism heading into December. As shown above, a four-month win streak not only has precedent (Sep-Dec 2015), but there was even a five-month win streak in the second halving cycle (Feb-Jun 2019). Combining this accumulation-phase trend with the aforementioned calendar-month trends as well as the potential for an approved US spot-BTC ETF, it is hard not to be optimistic about year-end PA.

All that said, there is no asset in history that goes straight up. At some point, BTC’s monthly price will in fact close lower than the month prior. I suspect this will occur in Q1 2024, but now is not the time for me to explain my prognostication. I will do so next month. For now, let us all just revel in current PA as long as it lasts.

On-Chain Data

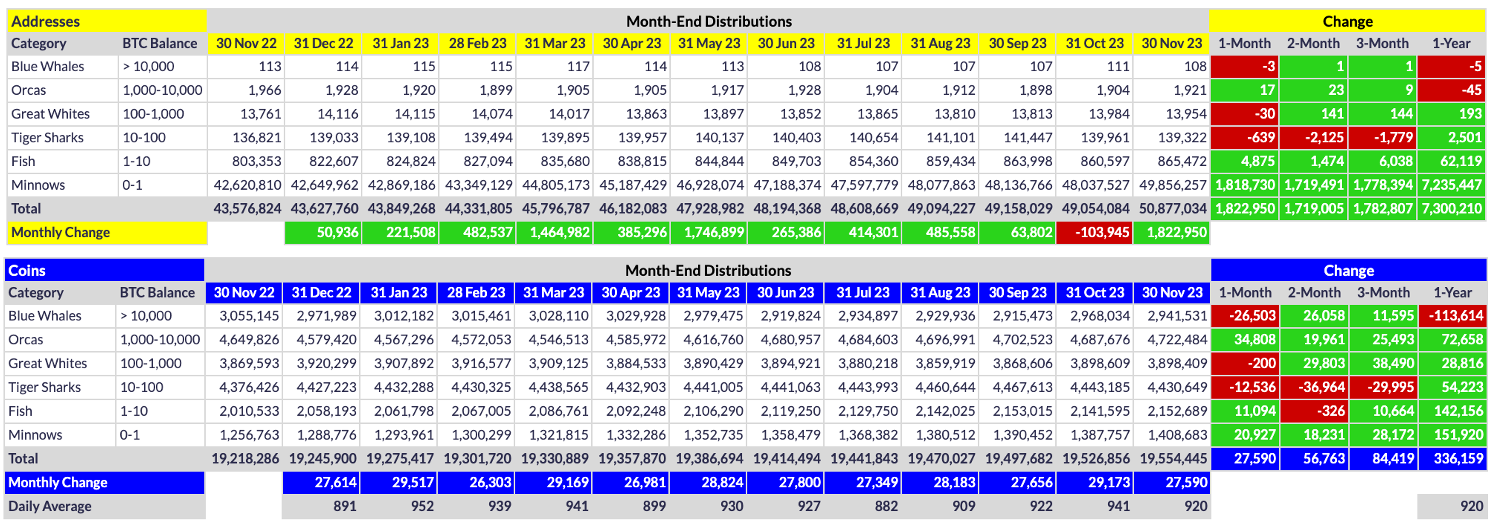

Below are the distribution of BTC addresses and coins for the past 12 months:

As shown above, retail buyers (Minnows & Fish) are on an absolute tear right now. A staggering 1.823M new retail buyers emerged this month, by far the largest one-month increase on record, surpassing the former one-month record set in May (1.746M). That said, three Blue Whales (BWs) devolved this month, their first contraction since June. Fortunately, the Orcas are finally showing some life, with 17 new Orcas in November, accumulating an impressive 34.8K coins in the process. This Orca increase (even after accounting for the BW losses) is likely responsible for price pushing 9% higher in November. On the other hand, I am convinced now more than ever that the BW selling that occurred in November was designed to keep a lid on price, not allowing it to exceed $38K for more than a minute. Why $38K was the magic number, I have no idea, but PA clearly exhibits market manipulation, and on-chain data lend further credence to this thesis. The most obvious explanation would be something related to the impending US spot-BTC ETF approvals that are likely to occur in January, but that is neither here nor there. Whatever the reason, BWs have decided that $38K will be the ceiling on price for the time being, and so it is.

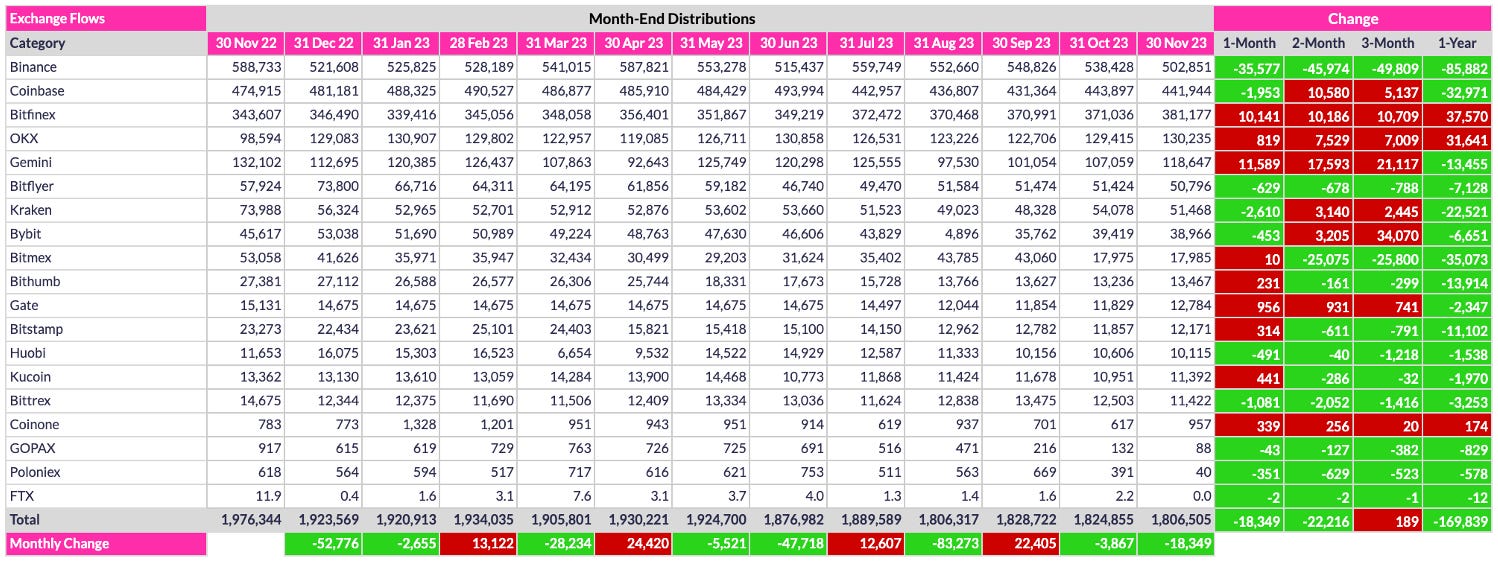

Price manipulation notwithstanding, some of the BW drawdown can be attributed to exchange outflows. As shown below, the listed exchanges experienced an 18.3K outflow in November:

Interestingly, coin flows varied considerably across exchanges, with, e.g., 35.6K coins flowing out of Binance, but 10.1K coins and 11.6K coins, respectively, flowing into Bitfinex and Gemini. The Binance outflows are undoubtedly due to US Department of Justice (DOJ) charges filed against Binance and its CEO, Changpeng Zhao, earlier this month. It is less clear why the latter two exchanges had such prominent inflows, although Bitfinex is a leading derivatives exchange, so that may account for their inflows (as institutional investors placed trades in anticipation of the US spot-BTC ETF application decisions). Whatever the case, some of the BW coin-loss can be attributed to exchange outflows, which is usually interpreted as bullish (as investors take coins off exchanges and put them into cold storage, those coins become less liquid/less likely to be sold in the near term).

Overall, outflows remain the predominant trend on most exchanges. In total, 170K coins have flowed out of the listed exchanges over the past year, which is a very positive trend indeed. While a complete dearth of coins on exchanges may still be years away, their near-continuous outflow does bode well for an eventual supply shock that could well send the price of a single Bitcoin into the stratosphere.

Other Thoughts

I have accumulated a number of thoughts over the past several months that I simply have been too lazy to post in long Twitter threads. However, I do think they are important to delineate because they will help clarify my investment outlook and strategy. Here are my thoughts in no particular order:

Trading vs. Hodling

As I state in my Twitter profile, I am a BTC maximalist in spirit but a profit maximalist in practice. What I mean by this is that I have ZERO doubt that BTC will one day be the preeminent store of value globally, and it may even become the world’s primary (or even sole) reserve currency. Whether full-on “hyperbitcoinization” ever occurs, there is simply no reason to question BTC’s future as the world’s preeminent store of value. Its attributes are simply far too superior to every other asset for the reasons I explain here. Its only drawbacks right now are volatility and complexity, but both of these drawbacks are ephemeral. User experience is improving by the day, and BTC will eventually achieve price equilibrium, though that time (and price) is likely a long way off.

My point is that I have full confidence in BTC’s future simply because it is superior to all other assets, and the rest of the world will realize this fact sooner or later. I also think it is the only cryptocurrency to be able to make this claim, simply because it is the only truly decentralized cryptocurrency. There are several other reasons I think BTC is superior to all other cryptocurrencies, but there are plenty of BTC maximalists who can beat this drum for me. No need for me to recapitulate the reasons here.

All that said, I am retired and have no sources of income other than investment income. I also retired relatively young (at 50; I’m now 54), and I still have two young boys at home (ages 12 and 10). As such, I need to generate income to offset my considerable non-discretionary expenses, and the way I do that is by trading. More specifically, I have a BTC stack that will hopefully remain in cold storage forever more, but I cannot rely on hodling alone to meet my monthly fiat obligations, particularly because of BTC’s volatility. As such, I trade part of my BTC stack (as opposed to only hodling), and I also trade many other cryptocurrencies because of their greater volatility. For example, I currently own a lot of ETH and SOL, and I have a small basket of mid- to low-cap altcoins. I know, anathema to a BTC maxi. But the last time I checked, BTC maxis aren’t offering to pay for my kids’ private school and golf tournaments, so get over it. i.e., I do not hold ETH, SOL or any other “shitcoin” because I believe in their long-term potential. I hold them because I believe their potential upside is greater on a percentage basis during bull markets. That said, they most certainly will be the first assets out the door when I think the market is peaking.

That is the other point I will address before leaving this general topic: selling at the market peak. First, NO ONE knows when any market will peak, least of all me. However, I do believe in the rhythm of the halving cycle, and there are a number of metrics that are pretty good at determining when BTC’s price is overextended. i.e., Until halving cycles fail to follow their repeated ebb and flow, there is simply no reason to try to countertrade them, regardless of what narrative has surfaced in the meantime (e.g., a halving cycle has never occurred during a US/global recession).

In any event, while it is unlikely I will catch the very top when I do sell, I have great confidence I can sell somewhere near the top, or more importantly, at a price far higher than the price I will eventually pay when I begin reaccumulating. I actually did pretty well last cycle in this regard, although I sold too late overall because I got too caught up in the hype of $100K BTC, the stock-to-flow model, etc. But I have learned my lesson and will forever more trust my instincts and experience. To that end, I absolutely nailed the cycle bottom, with my average reaccumulation price being $17.1K. I even bought the absolute nadir ($15.5K), something I am quite proud of given the din of $12K/$10K/$6K calls that were permeating CT at the time I was buying.

The long and short of it is that, yes, I am a BTC maxi in spirit, but until price reaches equilibrium (becomes substantially less volatile) and/or my kids are out of the house, I need to actively trade to put food on the table, and there are many assets better than BTC for the purposes of trying to maximize trading gains. This is the sole reason I own other cryptocurrencies (NB: I also own several BTC proxies in my retirement accounts because I cannot buy spot BTC - equities like MSTR, COIN, MARA, and GBTC. Whether I convert any/all of these upon ETF approval remains to be seen, but at the moment, my inclination is to remain diversified).

Risk-On vs. Risk-Off

Many talking heads out there still claim BTC is a “risk-on” asset, meaning that its price increases when investors are emboldened to take greater risks and decreases when they are inclined to be more conservative. The primary reasons these talking heads either implicitly or explicitly hold this view is because of BTC’s infamous volatility and its past correlation with other risk-on assets. While I understand this perspective and actually agreed with it at one time, I now think these same talking heads have failed to notice the changes that have occurred in BTC investor behavior over the past year. One example from early in the year is the PA that unfolded when Silicon Valley Bank (SVB) failed on March 10. BTC’s price ROCKETED over the ensuing week, from $20.3K to $28.2K (40%). i.e., Not only did BTC’s price not drop on such “risk-off” news, it actually skyrocketed.

Another example is the decoupling of BTC’s PA from risk-on assets like the Nasdaq (NDX). While BTC and the NDX traded directionally similarly (both up or both down) about 70% of the time between 2020 and 2022, they have traded directionally similarly only 59% of the time in 2023 and only 56% of the time since SVB’s failure. This recent correlation is barely above chance (i.e., Price will randomly trade directionally similarly 50% of the time). All of this is to say that BTC has unequivocally traded more like a risk-off asset than a risk-on asset over the past year.

The most recent example of BTC’s transition from risk on to risk off is its PA two weeks ago (on November 14), when US inflation data came in lower than expected. The diametrically opposed PA that day (BTC down 2.5%, NDX up 2.4%) is the clearest indication yet that BTC is now seen by many investors as a risk-off asset rather than a risk-on asset, just as I explained in my tweet that day. If true, then you as a BTC investor need to ask yourself this one question: what is your outlook for the global macroeconomy in the near term and over the longer term? The answer to this question matters more now than ever if indeed BTC is transitioning from being risk on to risk off. Below are my own thoughts on the matter.

US Consumer “Strength”

Despite what pop media have been reporting, the US consumer is NOT strong right now. Yes, a lot of people increased their savings balances during the pandemic, in part due to the deluge of stimulus payments that were provided, but also due to the fact that everyone was locked inside their house not buying $6 lattes on a daily basis. That surplus savings has bolstered recent consumer spending, but now those surplus savings have nearly evaporated. Moreover, debt payment postponements that were implemented during the pandemic (e.g., student loans and mortgage forbearance) have recently expired. With lower savings balances and much higher recurring expenses, it is little wonder consumer credit use just reached an all-time high and delinquencies on other types of credit (e.g., auto loans) are nearing an all-time high. i.e., US residents (and I suspect many other residents around the globe) are trying to maintain their current lifestyle despite the fact they no longer have the free cash flow to do so. History shows that many US residents will in fact use credit to maintain their lifestyle and even risk delinquency or default before finally reigning in spending. There is no reason to believe now is any different.

Given this intractable consumer behavior, combined with the relentless and exorbitant fiscal deficit spending of the US government (a form of economic stimulus), it makes sense that the US consumer appears strong right now (look no further than last week’s Black Friday sales data). The reality is, however, that US consumers are rotting from the inside out, so it won’t be long before sores begin to emerge. That said, there are still a number of US homeowners with substantial home equity, so expect that cohort of consumers to draw down their equity before they too are finally forced to throw in the towel. In short, US consumers have been kicking the can down the road for months now, and some may be able to kick it down the road a bit longer, but once all their savings are depleted, credit cards are maxed out, home equity lines drawn down and car repossessions in full swing, the US economy will get hit by the mother of all recessions. But that time is not now. Instead, we remain in limbo (or in the midst of a “soft-landing,” as the more delusional among us are wont to say).

Fed Funds Rate, Inflation, and Bond Yields

Many people have more expertise in this area than I do, but I have been investing long enough to have a pretty good grasp of these topics, particularly given that I believe we have experienced a secular change recently that very few active investors have experienced in their lifetime (we are end at the of a 40-year bond bull market).

In brief, the standard narrative presumes that inflation/disinflation/deflation drives changes in the US Federal Reserve (Fed) funds rate, which in turn induces changes in consumer interest rates and US treasury yields. For example, US inflation (as measured by the Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE) rate) started increasing rapidly in late 2021, so the Fed responded by (rapidly) increasing the Fed funds rate, which subsequently caused interest rates to rise for all sorts of loans, including auto loans and house mortgages. Moreover, because of the increase in Fed funds rate, treasury (bond) yields also increased, as investors now expected a higher return in exchange for their T-bill/bond purchases.

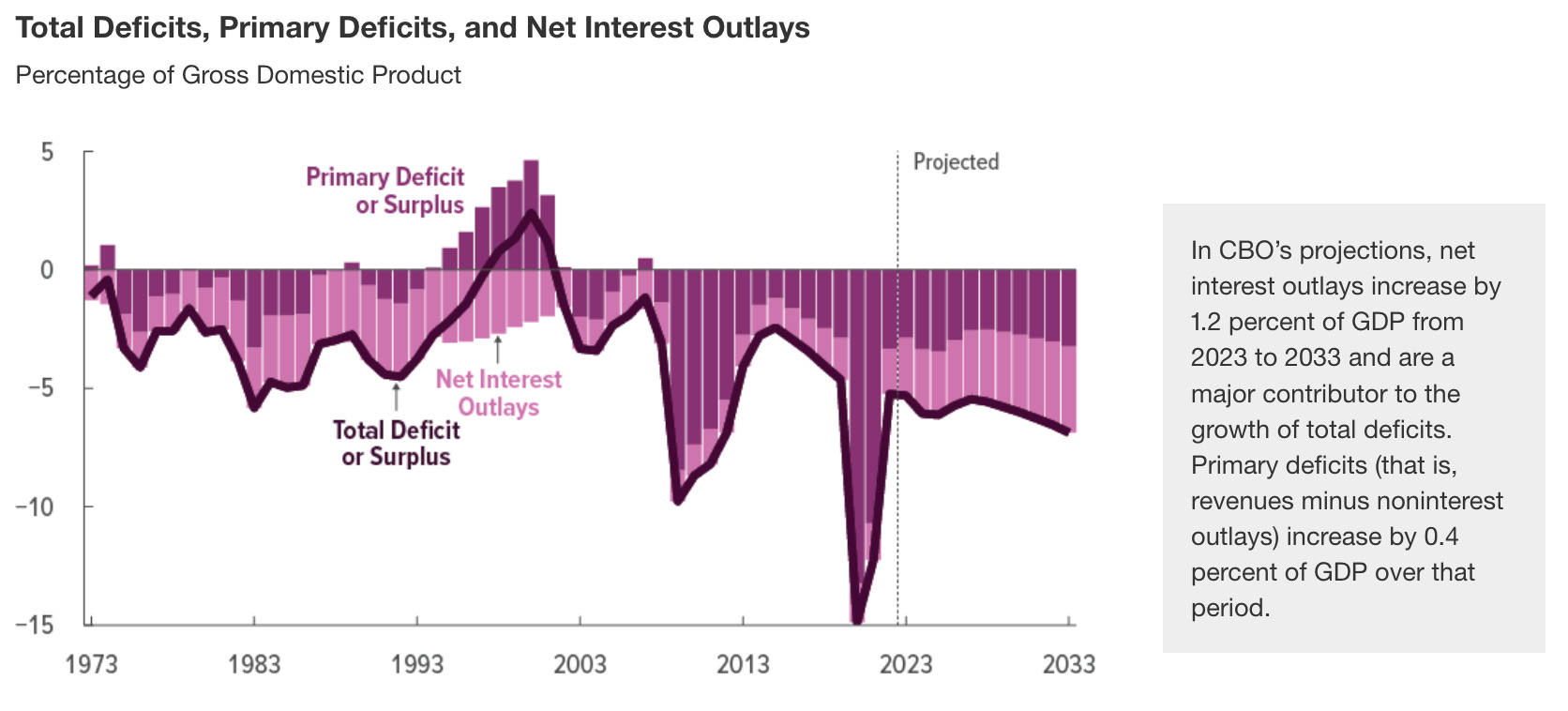

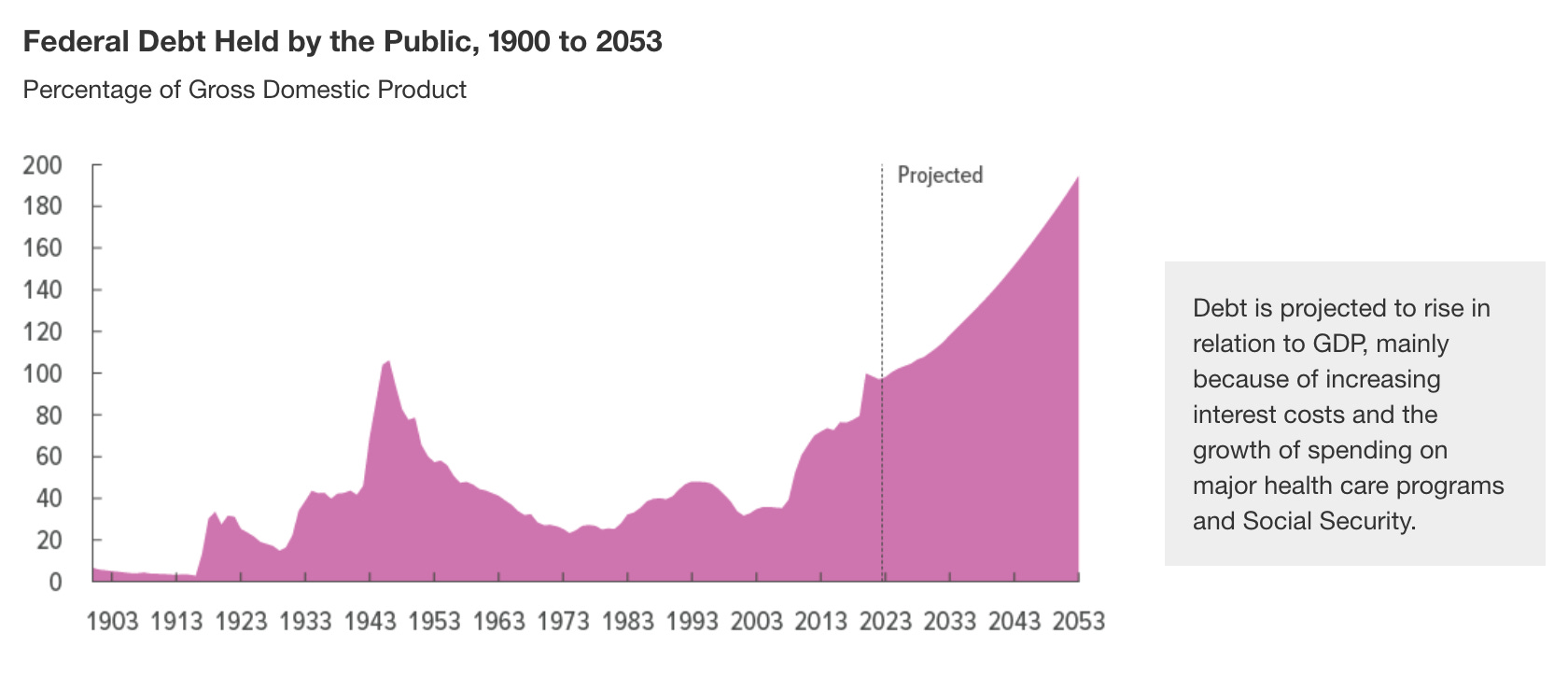

While this standard narrative has held true for the past 40 years, it likely will not hold true in the future. More correctly stated, although these same relationships will likely continue to hold true, there are now other factors that will impact inflation and bond yields, namely US fiscal deficit spending. As Lyn Alden has pointed out several times and others have pointed out as long ago as 2018, US fiscal deficit spending has never been this high in a non-recessionary period, and it has skyrocketed since the pandemic. Worse still is that even the Congressional Budget Office (CBO) is projecting annual budget deficits and cumulative federal debt to increase rapidly in the years ahead:

The reason I highlight these projections is because it is all but certain that bond yields will start rising (and likely rapidly) even if inflation subsides and the Fed subsequently starts cutting the Fed funds rate. Why? Supply and demand. While I will not take the time here to explain why bond prices and bond yields are inversely correlated (see my tweet here instead), the simple fact of the matter is that the US Treasury is going to issue FAR more bonds in the coming years that the total addressable market (TAM) can handle. First and foremost, the two largest international buyers of US treasuries (China & Japan) have already lost their appetite, and fewer and fewer US buyers are interested, particularly for long-duration bonds (e.g., 10-year, 30-year). There simply is too much macroeconomic uncertainty to assume such duration risk, which means the Treasury will be forced to not only offer more short-dated bonds than normally, but such rampant deficit spending is likely to force the Fed to eventually implement yield curve control (YCC), whether implicitly or explicitly. In other words, the Fed will likely become the buyer of last resort for US treasuries; they will be forced to monetize these runaway fiscal deficits.

The reason this is important is because, as we have learned acutely over the past three years (or really, since the Great Financial Crisis), whenever the Fed increases liquidity, whether by lowering the funds rate, offering swap lines, establishing “temporary” credit facilities like the Bank Term Funding Program (BTFP), or exercising quantitative easing by purchasing US treasuries and/or mortgage-backed securities, most assets increase in price, particularly “hard” (finite/limited-quantity) assets. BTC is a already one of the hardest assets on the planet, and it is about to become even harder after the next halving, so it will undoubtedly get a substantial price boost once the Fed starts increasing liquidity by whatever mechanism(s) it deems most palatable at the time.

In sum, US debt has (and will continue to have) much shorter maturity durations than in times past, so it will not only roll over sooner (maturities will arrive more quickly), but new debt will be issued at much higher rates due to a lack of demand. As such, interest expense on the debt will increase rapidly. i.e., Bond yields will skyrocket almost irrespective of Fed funds rate changes (even if the Fed pivots/begins reducing the Fed funds rate) simply because there will be insufficient demand for future bonds.

So What?

Those reading the sections above are no doubt asking themselves, “Fine, but what does any of this mean for the price of BTC?” Glad you asked, because the answer is one I am happy to report: BTC’s price will benefit greatly due to the unfortunate but inevitable US consumer collapse and increasingly irresponsible fiscal deficit spending.

Why? Because of the de facto response of the US Congress to all economic ills: more fiscal stimulus. As explained, such stimulus is good for most asset classes, but none more so than hard assets, and few assets are harder than BTC. Interestingly, however, the converse is also true: even if the US economy does not enter a recession (US consumers remains robust far longer than anyone can imagine), what will happen? Inflation. Rampant unmitigated and potentially uncontrollable inflation.

Higher inflation of course means higher Fed funds rates (and thus higher interest rates), at least while Jerome Powell remains Federal Reserve Chair. Recall the standard narrative above, that Fed “tightening” should be bad for BTC because the US dollar (USD) strengthens during periods of Fed tightening, which is bad for many asset classes. Again, this was once the case, but no longer, in my opinion. Why? Because, as I explained earlier, BTC is now seen by more investors as risk off rather than risk on. Again, look no further than BTC’s PA when SVB collapsed and when US inflation data came in below expectations. Neither PA would have unfolded three years ago, but it did this year.

In short, out-of-control inflation will benefit BTC regardless of whether the Fed raises rates because hard assets are the only antidote to truly rampant inflation. i.e., Even though the USD will initially strengthen (relative to other fiat currencies) when rates rise, which will likely depress BTC’s price in the short term, the USD will start losing purchasing power even more rapidly than it is now. And once bond investors lose confidence in the Fed’s ability to tame such rampant inflation, hard assets will be the only game in town, and no hard asset will be more attractive at that time than BTC.

Don’t believe me? Just look at countries that have experienced extreme inflation in the recent past (e.g., Turkiye, Nigeria, Venezuela, Argentina) and the commensurate hikes in interest rates. What do residents of such countries do when they receive payment/income in local currencies? They immediately convert them to a more stable alternative. Right now, USD stablecoins like Tether (USDT) are attractive because the USD is stronger and more stable than their own currencies, but what happens when the USD itself begins uncontrollably debasing/inflating? Gold? Ha. Gold has so many drawbacks in the modern world, it isn’t even funny. I will not recapitulate all of gold’s weaknesses as a currency here; see my article here for a more detailed explanation.

The answer of course is BTC. And we are already seeing evidence of this behavior. i.e., When USD stablecoins are no longer a viable alternative for people because the USD itself is inflating away uncontrollably, BTC will be the only viable alternative.

As I delineated above, BTC “wins” in both inflationary and deflationary (recessionary) environments. In fact, BTC wins in all scenarios except one: the US Congress/Treasury & Fed actually manage to thread their badly frayed yarn of fiscal and monetary policy through the pinhole-sized eye of the soft-landing needle. Put another way, unless you think US fiscal and monetary policy will suddenly, substantially and permanently improve, there is no scenario under which BTC does not win. The only question is when.

Trying to guess the timing of any macroeconomic event is a fool’s errand; there are simply too many variables that influence the economy. But you can certainly count me among the skeptics with respect to whether the US will suddenly change course and save us all from economic disaster. I just don’t see how they can. Even if US leaders suddenly started making more prudent fiscal and monetary policy decisions, it really does seem too late. The US debt is nearly $34 TRILLION and counting.

Granted, the federal budget is not equivalent to a personal budget, as many modern monetary theorists rightly state, but neither can US leaders wholly disregard US debt obligations, especially when interest rates are non-zero and the debt-to-GDP ratio is at record levels. Interest payments on the debt as a percentage of GDP are already high and rising, and that percentage will continue increasing heretofore whether the economy is in an inflationary environment (higher interest rates will increase the debt-to-GDP ratio even if spending is held constant) or a deflationary environment (tax receipts will fall, widening the deficit even if spending is held constant).

As if all of this isn’t enough, the world is also trying to reduce the role of the USD as global reserve currency. Again, international appetite for US treasuries has waned and other countries are taking additional steps to ease dollar dependence, like pricing oil in currencies other than the USD. As more and more countries try to eradicate the USD as the global reserve currency, the harder it will be for the US government to merely print USD to pay its ever-escalating interest expenses.

The bottom line is that the only scenario where Bitcoin does not benefit is the so-called soft landing scenario, where inflation drops back to 2%, the Fed lowers its fund rate to 2%, and the economy, even if it goes into recession, enters a mild and/or short recession. So really the only question you have to ask yourself is this: what is the likelihood of such a Goldilocks scenario? In my opinion, it is very very low, nigh impossible, both in the near term and over the long term, which is precisely why I am so heavily invested in Bitcoin.

In short, I have never been more convinced than I am right now that BTC will eventually become the preeminent store of value globally (but at a MUCH higher price than it is today). It simply has too many advantages over other stores of value, and there is no question the era of fiat-currency dominance is nearing its end.

Microstrategy (MSTR)

I still question whether MSTR continually adding to their stockpile is good or bad for BTC in toto, but one cannot question either their resolve or their thesis: would you rather own a highly volatile but highly appreciating asset or a more stable but continually depreciating asset?

To put the answer in perspective, below is a (crude) graph showing the change in BTC’s value since mid-2020, about the time MSTR started purchasing BTC, versus the change in value of USD over the same time period. Even when cutting the performance of BTC in half for 2020 (i.e., not cherry-picking the pandemic-induced bottom as a starting point nor including the entire 304% annual rate of return that year), $100 invested in BTC in 2020 would be worth about $340 today, whereas the same $100 held in USD would be worth about $82 today given the ravages of inflation (the dotted orange line is BTC’s value trend line with volatility smoothed out).

So tell me, Alexander Stahel, who exactly is insane? MSTR or, e.g., investors sitting in USD the past three years or, heaven forbid, buyers of “risk-free” US treasuries?

US Spot-BTC ETF

For what it’s worth, I do not think approval of a US spot-BTC ETF is already priced in. The reason is simple, as I explained in response to a PlanB tweet: if you believe the primary investor pool for an approved ETF is institutional money, investors who cannot currently invest in BTC without an ETF vehicle, then ETF approval is not - indeed CANNOT - be priced in. That pool of cash is still involuntarily but necessarily sitting on the sidelines. I personally fall in this camp.

That said, I do not know how large the waiting pool of capital is, and that is what tempers my expectations regarding a post-approval price pump despite the prognostications of some ETF uber-bulls. i.e., I fully believe price will skyrocket the moment ETF approval is announced, but whether that pump sustains will depend on two factors: 1) the gap in time between approval announcement and actual launch; and 2) how much new capital is ready/willing to invest upon launch. I can venture a reasonable guess about the first factor (I have read it could take up to 75 days to start trading, but my guess is 30 days or less). I cannot, however, offer a reasonable guess about the latter factor, and that obviously is the most important factor. If there isn’t a tsunami of capital waiting to be invested, then any post-approval price pump will undoubtedly waver and potentially even retrace quite substantially.

Whatever the reality, I do not think ETF approval will be a “sell the news” event. Anyone spouting such nonsense is either engagement farming or clueless. I have seen people trying to equate, e.g., the COIN IPO with the impending US spot-BTC ETF. I can hardly think of a more misguided comparison. While Coinbase obviously benefits from BTC trading, the idea that an exchange going public would have any direct positive correlation with an asset’s price is ridiculous. That would be like AAPL pumping upon the announcement of Etrade’s IPO. One event hardly has anything to do with the other.

Conversely, there can literally be no more direct correlation than a spot-ETF and its underlying asset. A spot-ETF’s sole raison d'etre is to buy the underlying asset! So no, ETF approval will not be a sell-the-news event. More correctly stated, there could be a dip in price if there is a long lag between approval and launch, particularly if the announcement induces an initial price spike, but the launch itself can be nothing but positively correlated with the underlying asset. Again, the concern I have is a lack of demand, and that is a non-trivial concern, in my opinion.

For example, if the status quo is maintained in macroland until the launch (inflation continues easing, there are no major economic crises, the DXY stabilizes, bond yields stabilize, etc.), then the launch could “flop” relatively speaking. i.e., Inflows could be tepid and/or take longer to materialize than expected, either/both of which would stifle any rally or perhaps even put downward pressure on price.

Still, even under this scenario - where capital inflows are overestimated - it does not mean ETF approval/launch will be a sell-the-news event. It merely will indicate that bulls have longer to wait for the bull market to resume (e.g., post-halving). And as far as I am concerned, that would be fine, even desirable. Gaining too much too quickly, which frankly I think has been case in 2023, makes such gains less sustainable over the long term. On-chain data support my concern as well, as I have explained over the past several months. i.e., Current price gains have happened primarily because the market was extremely oversold at the end of 2022 and because BTC has recently been transitioning from a risk-on asset to a risk-off asset. However, Orca growth has been tepid this year and BWs have been sellers of late, neither of which is conducive to a substantial and sustainable price pump. Contrast these on-chain data trends with those of, e.g., late 2020 and early 2021, when more than 400 new Orcas joined their pod within six weeks. Now that was a true bull market. The current market, while bullish price-wise, is decidedly less bullish from an on-chain perspective.

Regardless, there is no scenario under which ETF approval/launch will be a sell-the-news event. Price may not substantially or sustainably increase following announcement/launch, but it most certainly will not swoon. Yes, price could consolidate for a while thereafter, especially if approval announcement leads to a parabolic spike prior to launch, but to suggest, e.g., price will plummet to $25K (or even lower) post-launch is absurd. Not going to happen.

NB: Most people who follow me know I rarely take such strong positions, but this is one time where I feel completely comfortable doing so. If price is to revisit mid- to low-$20K again, it will be due to some unforeseeable cataclysm, NOT because of the approval/launch of a US spot-BTC ETF, especially when we are only a few months away from the next halving.

If one is seeking a legitimate precedent for what BTC PA might look like post-ETF launch, then GLD’s launch is a far better comparison. Ironically, the biggest spot-BTC ETF bulls are fond of citing how much GLD’s price increased after its launch. True. But not immediately. If you look at PA the first six months post-launch (November 2004 to May 2005), you will see that price actually retraced about 9% (from $45 to $41) before finally finding its footing:

If a US spot-BTC ETF were to trade similarly, price would chop lower during the first half of 2024 (e.g., from $38K to $34K) before reversing and going on a parabolic run.

NB: I am NOT stating that I think this is the most likely outcome. I am merely pointing out that GLD is the only legitimate referent for trying to predict BTC PA following ETF approval/launch. As I mentioned, I personally think price will spike upon approval, consolidate shortly thereafter (until the time of actual launch), and then… who knows. It will all depend on capital inflows, both timing and amount.

Conclusion

November 2023 was another impressive month for BTC, both in terms of PA and network adoption. Furthermore, the outlook for both price and network adoption has arguably never been better than right now, which causes me to be particularly bullish going into December. That said, I have been investing way long enough to know that anything can happen at any time, and particularly in Bitcoinistan. I have seen market sentiment turn on a dime many many times, so it certainly could happen again in December. All it would take is some crypto-specific or macroeconomic fear, uncertainty and doubt (FUD), and wham! That said, barring something completely unforeseeable, there is every reason to be optimistic about the month ahead. Whether due to relative Fed dovishness, seasonal trading patterns, the rhythm of the halving cycle or the impending approval of one or more US spot-BTC ETFs, December 2023 looks like it will be a month to remember. And hopefully for positive reasons. :-)

Go #BTC.