Month-End Analysis

Disclaimer

The data I use (BitInfoCharts, Coinglass, CoinMarketCap) to compile the tables and graphs contained in the on-chain section of this analysis do not always align with data found via others sources like Glassnode and CryptoQuant. I cannot explain the reason for the differences nor can I confirm which sources are most accurate. For this and other reasons, I have come to trust only the on-chain data I collect when trying to explain and/or predict Bitcoin’s (BTC) future price action (PA). Whether you too find my on-chain analysis useful is for you to decide, but I can assure you that some of my observations and/or predictions will differ, often markedly, from other observations and/or predictions you will see on Crypto Twitter (CT) and elsewhere.

Price Action

September PA was both less volatile and more bullish than many people expected. Price opened at $25,935, reached a peak of $27,488 on September 19, and then closed the month at $26,968, a full 4.0% higher.

Although September is unquestionably a bad month for BTC historically speaking, most of you know I personally think price predictions based on calendar months have little validity. Instead, I think the rhythm of the halving cycle is far more important in predicting price, which is why I predicted last month that price would increase in September despite the six-year losing streak, and it did.

As shown above, we are in what I call the accumulation phase of the halving cycle, which is the 13-16 month period before the next halving. As illustrated, this phase of the halving cycle is a mix of up and down months but with the phase skewing more bullish than bearish overall. Hence the reason I predicted this September would end higher: only once before has price closed lower three consecutive months during the accumulation phase (Jul-Sep 2019), and that was because of the incredible runup that preceded it the first half of 2019. i.e., Although the first half of 2023 has also been bullish (peaking at 92% higher in mid-July), the runup the first half of this year pales in comparison to the 271% runup that occurred in H1 2019.

The question now then is what I think will happen in October. Hard to say. I can see price going either way. i.e., Despite the bullishness surrounding October (“Uptober” anyone?), again, I think assuming price will go higher in October simply because it has more often than not in past Octobers is silly. Instead, I refer back to the accumulation phase of the halving cycle. In so doing, it wouldn’t surprise me if October were to close lower. After all, price is already up 63% year-to-date, which is a very good year by any measure, and the red streak of July and August has now been broken. As such, a red October seems reasonable. On the other hand, only four of the first nine months of this accumulation phase have closed higher, so several more green months before the next halving is to be expected, so...

Because a case can be made for both the bulls and bears in October based on the rhythm of the halving cycle, another place to look are BTC’s quarterly returns during previous accumulation phases:

As shown above, the first two quarters of 2023 closed 72% and 7% higher, respectively, while Q3 just closed 12% lower. Looking at the quarterly returns of the accumulation phases of previous cycles (in black boxes) shows that about half of the quarters closed higher while half closed lower (though the green quarters closed substantially higher than the red quarters closed lower). If this trend were to continue for this cycle, then at least one of the next two quarters will close lower (NB: the current estimate for the next halving is April 2024, so two quarters remain before the next halving). Given the current macro environment and continued delays in getting a spot-BTC exchange traded fund (ETF) approved in the US, I would bet Q4 2023 is the quarter that will close lower before a rebound in Q1 2024. If so, then I predict at least two of the next three months will close lower. Whether those two months end up being October and November, October and December, or November and December, I have no idea. But I do think two of the next three months will close lower, as will the quarter overall.

Note of course I have no idea what will actually happen. None. I am basing my predictions solely on the rhythm of the halving cycle, and while I personally have great confidence in this rhythm, I am also familiar with all of the counterarguments for why the halving cycle no longer matters (or perhaps never did). I also recognize that changes in the global macro environment can/will exert influence over the BTC market. But that is neither here nor there. None of this is financial advice. I am merely sharing my opinion based on the rhythm of halving cycles and in the absence of any significant changes in the global macro environment.

On-Chain Data

Below are the distribution of addresses and coins for the past 12 months:

As shown above, address expansion continues across virtually all tiers except, importantly, the Orcas. As I explained here and here, I think Orca growth is the only way price can substantially and sustainably increase. At current price levels, retail buyers simply do not have the purchasing power to meaningfully move price higher. Nevertheless, it is impressive to see retail buyers (Fish and Minnows) have monotonically increased for the past 12 months. That said, there was a substantial contraction among Minnows at the very end of the month, a contraction for which I have yet to find an explanation. At their peak (on September 23), Minnows had expanded by 858K for the month. However, as shown above, they closed the month “only” 58.9K higher in number, meaning nearly 800K Minnows vanished the final seven days of the month. The bleed has continued into October as well, so this is definitely something to keep an eye on. Retail interest in BTC has done nothing but expand exponentially the past several years, so to see a severe contraction, especially over such a short period of time and for no obvious reason, is a concern indeed.

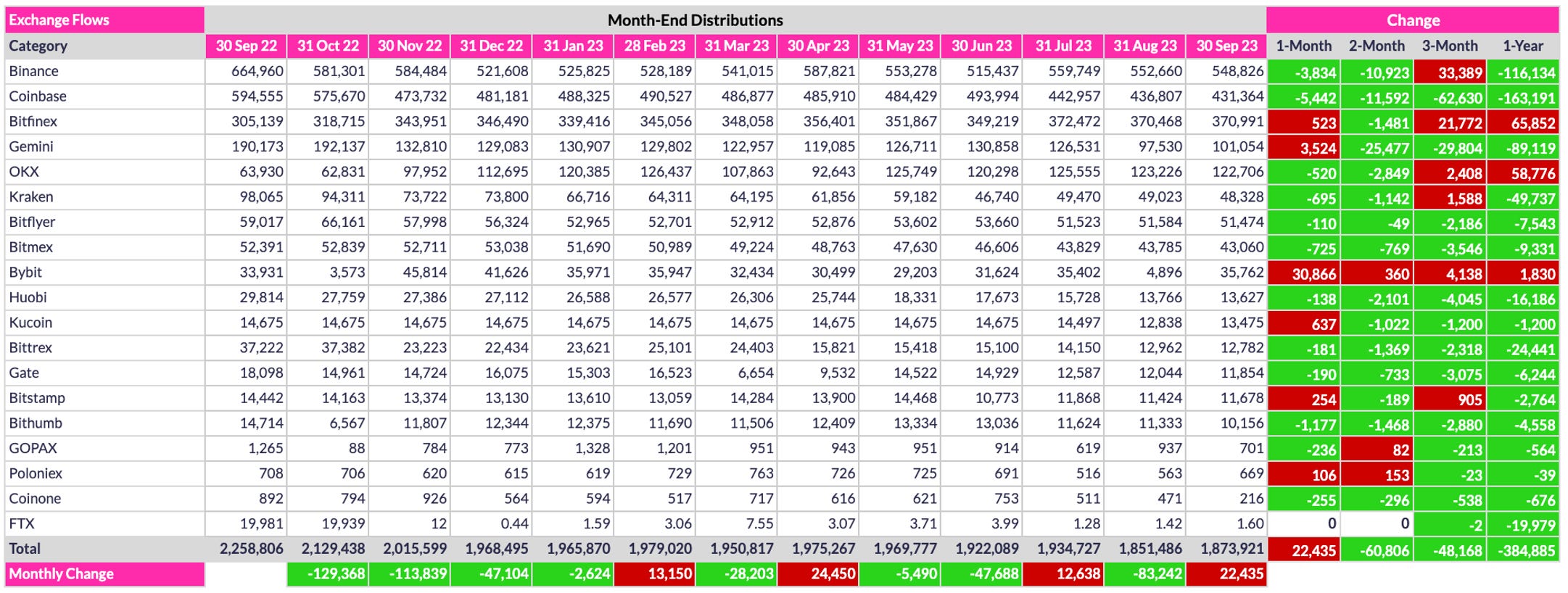

Below is a table reflecting exchange inventories for the past twelve months:

As shown above, listed exchanges experienced a combined net inflow of 22.4K coins in September. This is the second month of the quarter that coins flowed into exchanges, though the net quarterly outflow remained a robust 48.2K coins overall. Note, however, that the September “inflow” is likely just a data-error correction by Coinglass for Bybit’s inventory. If so, then September actually experienced an 8.5K outflow overall as opposed to a 22.4K inflow. Regardless, the longer-term trend is clear: the exchanges above now have 385K fewer coins than they did at this point last year. At that rate of outflow, exchanges will be devoid of coins in less than five years. Think about that.

Conclusion

September 2023 was mildly bullish, closing 4% higher, but it was much more bullish than most had anticipated. Conversely, I think October is as likely to close lower than higher despite the prevailing “Uptober” sentiment on CT and elsewhere, if for no other reason than the usual ticking time bombs in macro land - increasing interest rates, threats of recession, a strengthening USD (at least relative to other fiat currencies). Conversely, there is one bullish catalyst on the horizon, and that is an approved spot-BTC ETF in the US. While I personally think approval is a foregone conclusion at this point - it is only a matter of when rather than if - how much of a price catalyst it would be depends on a couple of factors.

First, as I pointed out in June, I think there will be a sizable pump upon news of the approval as well as when the ETF first launches. However, I do expect the first pump to retrace quite a bit following the initial euphoria because there will likely be a sizable period of time between when the application is approved and when the fund(s) actually open for trading. Perhaps more importantly, however, is that market sentiment will matter A LOT when the fund(s) start trading. i.e., I personally want ETF approval delayed as long as possible, ideally until late Q1 2024. Why? Because the halving narrative will kick into high gear in early 2024, so having a US spot-BTC ETF approved around that time would be a synergistic catalyst to propel price into the stratosphere. Conversely, if an ETF were approved, e.g., this coming month (in October), there will be FAR less mainstream investor interest. i.e., Yes, perhaps up to $1B will flow into the ETF initially, but nowhere near as much as there would if mainstream interest in BTC were higher, and that simply isn’t the case right now. Hardly anyone outside us lunatics has any interest in the corn right now. We need mainstream interest to rekindle BEFORE an ETF is approved. Otherwise, the initial pump, post-approval, will not only be much milder than anticipated but also less sustainable. There is no doubt in my mind.

I’ll conclude this month’s analysis on that happy note, LOL. Hope everyone is well.

Go #BTC.